🛡️Insurance Companies

1. Introduction to the Insurance Sector🛡️

1.1. History and Evolution of the Insurance Industry 📜

The concept of insurance is not a modern invention; its roots extend to early civilizations. In Mesopotamia, for example, the Code of Hammurabi, dating back to around 1750 BC, already contained rudimentary clauses regulating liability and commercial risks, protecting merchants and their goods against eventualities such as theft or disaster during transport. Similarly, in ancient Rome, organizations like the collegia funeraticia and military compensation systems offered an early form of social security, providing compensation for accidents and deaths. These systems not only ensured the well-being of injured soldiers or the families of the deceased but also provided access to essential services for the lower classes, laying the groundwork for what is now known as life and occupational accident insurance.

A significant turning point in the history of modern insurance was the Great Fire of London in 1666. This disaster devastated the city, highlighting the fragility of assets and the urgent need for a formal financial protection system. This event catalyzed the creation of the first fire insurance companies, setting a precedent for the insurance industry. From then on, the sector began to consolidate in the 18th century, with the expansion and diversification of products to include life, fire, and marine insurance. Legal entities such as London Assurance and Royal Exchange Assurance emerged, establishing standards and improving public confidence in the sector.

The Industrial Revolution in the 19th century radically transformed the economy, driving the growth of new types of insurance adapted to emerging risks. The expansion of cities and the development of technologies required adequate protection against accidents, fires, and theft, leading companies to offer customized policies for booming industries. During this period, government regulation became necessary to protect consumers and formalize the commercial practices of insurers, laying the foundations for a more robust legal framework.

The 20th century witnessed further diversification and modernization. With increased social awareness and changes in modern life, health, automobile, and civil liability insurance emerged, adapting to the new protection needs of citizens. Health and life insurance, in particular, became critically important in helping families manage the financial risks inherent in modern life.

Finally, the 21st century has brought a technological revolution that has transformed the industry. Digitalization has enabled policy customization, driven a growing focus on sustainability, and highlighted the vital importance of cybersecurity as an emerging risk and opportunity for the sector.

The history of insurance demonstrates a remarkable capacity for adaptation over time. From its rudimentary origins to today's sophisticated industry, the sector has consistently reinvented its offerings and operating models in the face of profound economic, social, and technological changes. This intrinsic adaptability gives the insurance sector inherent resilience, making it a potentially stable long-term investment. Unlike other industries that may become obsolete, the fundamental human need to manage uncertainty and transfer risk is constant, and insurers have repeatedly demonstrated their ability to meet it in new ways.

Furthermore, the historical evolution of the sector underscores a crucial aspect: regulation. The need for regulation, as observed in the 19th century, was not simply a burden, but a decisive factor in building public trust and formalizing the industry. Without a solid regulatory framework, the sector's growth and legitimacy could have been hampered by instability or fraud. This symbiotic relationship between regulation and industry growth implies that while regulations can impose costs or restrictions, they also provide the necessary structure for stability, transparency, and consumer confidence—vital elements for a business built on long-term promises. For investors, a well-regulated market mitigates systemic risk and fosters a more predictable operating environment, even if it limits explosive short-term gains.

1.2. Key Characteristics Making it Attractive for Investment ✨

The insurance sector presents several intrinsic characteristics that make it attractive to investors seeking stability and long-term growth potential.

One of the most notable advantages is high barriers to entry. The need to comply with rigorous capital requirements, the demand for deep risk management expertise, and the complexity of regulatory compliance act as a protective moat for established players in the industry. This limits the emergence of significant new competitors and contributes to less market fragmentation in many segments.

Insurance policies, which involve the recurring payment of premiums, generate stable and predictable revenue streams for insurers. This revenue stability, combined with prudent management, often allows companies to offer attractive dividends to their shareholders, making them an interesting option for investors seeking passive income.

Although not immune to economic cycles, the insurance sector tends to show relative stability compared to other more volatile industries. The demand for insurance, especially for essential risks such as health or property, is less elastic to economic fluctuations, providing a more resilient revenue base.

Capital management and solvency are fundamental pillars in evaluating an insurer. A company's ability to meet its long-term financial obligations is essential for its stability and the confidence of policyholders. This financial strength is reinforced by the composition of its investment portfolio. Insurers invest a significant portion of their assets in cash, deposits, and fixed income (around 72.6%), with a considerable portion (48.1%) in government debt and 18% in equities. This portfolio composition is crucial for maintaining the company's solvency and liquidity.

A distinctive and advantageous feature for insurers is what is known as the "float advantage." Insurers collect premiums upfront (the "float") before they have to pay claims, which can occur months or even years later. This "float" is, in essence, interest-free capital that insurers can invest. An insurance company's profitability is therefore a combination of its underwriting profit (premiums minus claims and expenses) and its investment income derived from this float. A company with solid underwriting can generate profits even with modest investment returns, while a company with poor underwriting might rely heavily on investment income, which increases its risk profile. For investors, understanding the size and management of this float is as important as analyzing underwriting performance.

Regulation, though often viewed as a limitation, acts as a barrier to entry and a mark of quality in the insurance sector. Strict regulations, high capital requirements, and the complexity of regulatory compliance deter new competitors, creating a kind of "moat" protecting established players. This can result in a less competitive market structure, allowing consolidated insurers to maintain potentially higher margins and more stable market shares. For investors, this translates into a more predictable competitive landscape and potentially more sustainable long-term returns.

2. Business Models in the Insurance Sector 🏢

2.1. Life Insurers 💖

Within this category, there are various types of policies:

-

Death Insurance: Offers compensation to beneficiaries in the event of the insured's death. Multiple variations exist within this type to adapt to different needs.

-

Survival Insurance: The insurance company commits to paying a periodic amount (annuity) if the insured lives for a predetermined period, or a deferred capital if the policyholder is still alive at the end of the agreed term.

-

Mixed Life Insurance: Combines elements of death and survival insurance, guaranteeing a benefit whether the insured dies or survives the term of the contract.

-

Unit-Linked Products: These are life policies that incorporate an investment component. They combine a risk-life insurance with the potential for returns from stock markets, where the policy's value is linked to the performance of underlying investment funds.

Europe: Allianz (ALV.DE) in Germany and AXA (CS.PA) in France, though diversified, have very strong life divisions. In Spain, Mapfre (MAP.MC) also has a significant life insurance area.

2.2. Non-Life (General) Insurers 🏠

Non-life insurers, also known as general insurers, focus on covering people and inanimate objects against a wide range of risks. Unlike life insurance, their contracts are usually renewable periodically, often annually.

They are mainly divided into two broad categories:

-

Property and Casualty Insurance (Seguros de Daños): Their objective is to cover the assets or patrimony of a person or company against risks and threats, aiming to repair financial loss when a claim occurs. Within this modality, there are different application forms, such as pro-rata, new-value insurance, and first-risk insurance. Common examples include fire insurance, civil liability insurance (which can arise from vehicle use, be general in nature, or cover professional errors and omissions), automobile insurance, agricultural insurance (covering risks to crops, animals, or hail), various pecuniary loss insurance (such as credit or bond insurance, or loss of profits), and theft insurance.

-

Service Provision Insurance (Seguros de Prestación de Servicios): In this type, the insurer commits to offering one or more specific services stipulated in the policy if the insured needs them. Examples of these insurances are health assistance, funeral expenses (covering funeral costs and services), legal defense, and travel and tourist assistance.

The distinctive characteristics of this business model include the short-term and renewable nature of their contracts, which implies a constant need for policy renewals and active acquisition of new customers. Furthermore, they are more exposed to claim volatility due to the occurrence of unexpected and large-scale events, such as natural catastrophes or mass accidents. This volatility directly impacts their loss ratio. Therefore, efficiency in managing operating and claims costs is crucial for maintaining profitability in this segment.

Claims Risk (Riesgo de Siniestralidad) is the main driver of profitability and, at the same time, of volatility for non-life insurers. Since these policies cover "inanimate objects" and "property and casualty insurance" and are generally short-term and renewable contracts, the core profitability of these insurers largely depends on the frequency and severity of claims that occur in a relatively short period. This directly impacts the "Loss Ratio."

Europe: Zurich Insurance Group (ZURN.SW) in Switzerland and Generali (G.MI) in Italy are major players in the non-life sector. In Spain, in addition to Mapfre, Catalana Occidente (COG.MC) is a good example.

China: Ping An Insurance (2318.HK) is one of the largest and most diversified insurers, with a significant non-life portfolio.

2.3. Auto Insurers 🚗

The most common types of coverage they offer include:

-

Civil Liability (Third-Party Liability): Covers costs associated with damages the insured may cause to other people or property while driving.

-

Physical Damage Coverage: Covers damage suffered by the insured's own vehicle, whether due to accidents, vandalism, or natural disasters.

-

Uninsured/Underinsured Motorist (UM/UIM): Protects the insured in case of an accident with a driver who does not have a policy or whose coverage is insufficient to cover the damages caused.

-

Personal Injury Protection (PIP) and Medical Payments (Med Pay): Help cover medical costs arising from an accident, regardless of fault, including hospital expenses, rehabilitation services, and even loss of income.

The business model of these insurers is characterized by a strong customer proximity, seeking personalized, flexible, and agile service through office networks, agents, and the use of technology. They prioritize efficiency and pricing discipline, which involves exhaustive monitoring of operating and expense indicators, and rigorous rate setting to ensure profitability.

Innovation is an important pillar, with flexibility to adapt the model to different markets and customer needs. A notable example is the implementation of behavior-based insurance, which uses telematics and vehicle data to adjust premiums according to the insured's driving habits.

Telematics and Big Data are transforming risk assessment and pricing in auto insurance. The explicit mention of "Behavior-Based Auto Insurance" that uses "telematics and vehicle data to adjust premiums" signals a fundamental shift in risk assessment, moving from traditional assessment (demographics, vehicle type) to one based on granular, real-time data. This technological advance allows insurers to price risk with greater accuracy, reward safer drivers, and potentially reduce claims by incentivizing better driving behavior. For investors, companies that successfully implement and leverage telematics data are likely to achieve lower loss ratios and higher profitability, gaining a competitive advantage. This also opens opportunities for new revenue streams through data-driven services and personalized offerings, although it requires significant investment in data analytics and cybersecurity.

United States: Progressive (PGR) and GEICO (part of Berkshire Hathaway - BRK.A) are known for their focus on innovation and telematics.

Europe: Admiral Group (ADM.L) in the UK is a major player and has been a pioneer in the use of telematics data.

Spain: Mapfre (MAP.MC) and Línea Directa Aseguradora (LDA.MC) have a significant market share in auto insurance.

2.4. Health Insurers 🏥

The main purpose of health insurers is to guarantee the insured the provision of medical services in case of accident or illness, which includes medical, surgical, pharmaceutical care, and hospitalization.

Currently, a new role is being proposed for these companies, going beyond their traditional administrative function (managing questionnaires, premiums, co-payments, and authorizations). The objective is to evolve towards a patient-centered approach, where the insurer genuinely cares about the health of its policyholders and facilitates access to the best medical resources. This implies a shift in focus towards the client's pathology, considering their medical history, current treatments, and preventive medicine.

A new health insurance model is based on several fundamental principles:

-

Interactivity, Online Health, Mobility, and Accessibility: The need for digital systems (apps and web platforms) that allow users to manage their health services "in the palm of their hand" is recognized, significantly improving the user experience.

-

Unified Personal Health Record: The integration of clinical information from clients and providers is a priority objective. This implies automatic data upload, strict control of access permissions, and the possibility for professionals to download reports for their own clinical records.

-

General Prescription Repository: The creation of accessible databases for insurers and professionals is key to streamlining authorizations and appointments, eliminating "unbearable" bureaucracy for the user.

-

Health Assistants: The need for intelligent assistants (such as chatbots or AI-based systems) is foreseen to guide users with accurate information on symptoms, pathologies, treatments, doctors, and how to access services.

-

New Relationship between Professionals and Insurer: The current fee-for-service model is considered obsolete. An evolution towards a collaboration that provides greater added value is proposed, with improved information for providers, promotion of online services, and encouragement of video consultations.

United States: UnitedHealth Group (UNH); CVS Health (CVS) (through its Aetna division); Elevance Health (ELV); Centene Corporation (CNC); Humana (HUM); Cigna Group (CI); Molina Healthcare (MOH).

When you see "Blue Cross Blue Shield" or "BCBS", keep in mind that it is not a single company. It is a federation of 34 independent, licensed health insurance companies, most of which are mutually owned or non-profit. Many companies (like Elevance Health) are part of this network and have their own stock exchange listings.

2.5. Specialty Claims Insurers 🚨🎯

Specialty claims and niche insurers are dedicated to offering protection against complex, emerging, or very specific risks that are often not addressed by traditional policies or that conventional insurers consider too difficult, high-risk, or unprofitable. This segment of the insurance market is a direct response to the evolving risk landscape in the modern business environment and the needs of very specific markets.

Among the most relevant coverages they offer are:

-

Cyber Risks: Protects businesses against costs arising from information theft or ransomware, digital fraud, cyber extortion, and business interruptions caused by cyber incidents.

-

D&O (Directors and Officers): Covers financial losses incurred by the company due to unfavorable decisions made by its directors or senior executives.

-

VCAP (Venture Capital): Protects companies against financial losses resulting from high-risk investments in startups, innovation projects, or strategic acquisitions.

-

Crisis and Sovereign Risk: Ensures a company's stability against political and regulatory risks, such as government-imposed measures.

-

Microinsurance for Online Purchases: Offers coverage for specific transactions made on e-commerce platforms, protecting the consumer against potential fraud, shipping damage, or even product dissatisfaction.

-

On-Demand Insurance for Electronic Devices: Allows users to activate or deactivate coverage based on actual device usage, optimizing cost and coverage.

-

Cancellation Insurance for Events and Travel: Provides refunds for cancellations related to unforeseen circumstances, such as illness or travel restrictions.

-

Excess and Surplus Lines (E&S): Specialize in property, casualty, and specialty risks that are "hard-to-place." This includes businesses with poor loss histories, high-risk locations, new or hazardous operations, and accounts requiring flexible terms and conditions or highly customized coverage (e.g., cannabis-related businesses, vacant buildings, etc.).

The business model of these insurers is based on deep underwriting expertise and personalized advice, analyzing the specific needs of each company or niche to recommend the ideal coverage. They often operate as brokers or intermediaries, allowing them access to multiple insurers and offering the best market options through strategic alliances. They focus on optimizing costs and coverages, designing plans that avoid unnecessary expenses and ensure optimal protection. Efficient claims management is a pillar, providing support throughout the process, from notification to resolution, and even intervening if the insurer does not respond in a timely manner. In addition, they use data intelligence to recommend the most suitable coverage in terms of costs and benefits.

By operating in less competitive segments, these companies can charge higher premiums for their specialized expertise. Although these risks are inherently higher, the ability to price them accurately and manage claims effectively can lead to superior underwriting profits compared to more commoditized insurance lines.

Examples of prominent listed companies in this segment include:

United States:

-

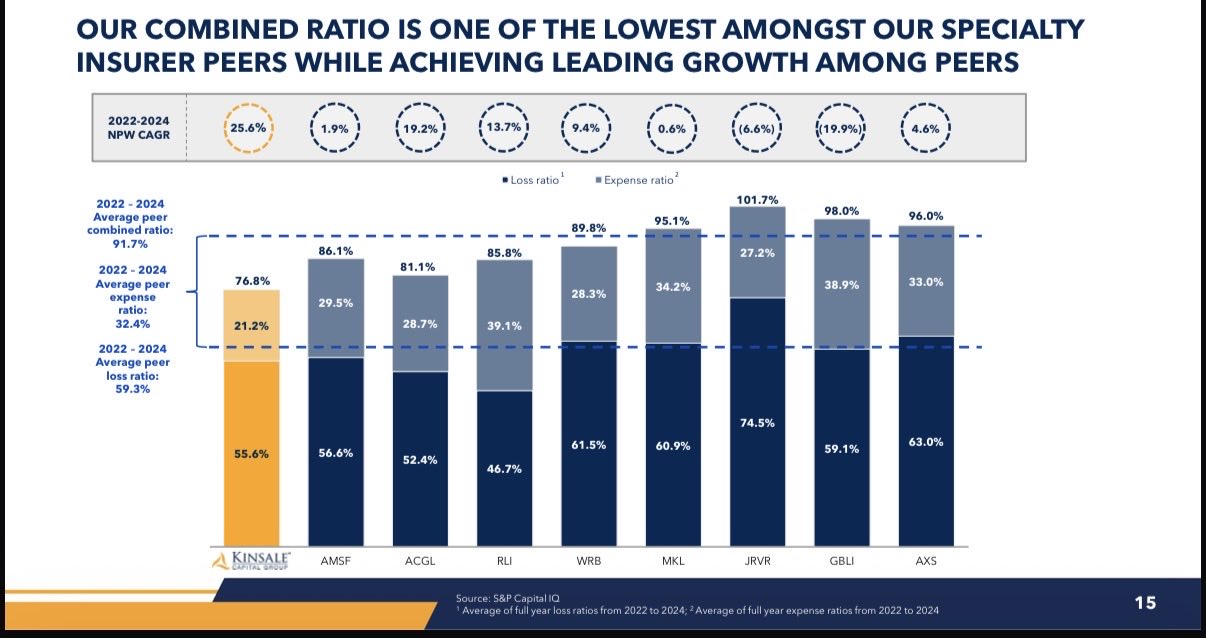

Kinsale Capital Group (KNSL): A clear example of a company operating in the U.S. excess and surplus lines market, specializing in "hard-to-place" risks for small to medium-sized accounts, allowing for great flexibility in its products and pricing.

-

International General Insurance Holdings Ltd. (IGIC) (listed on NASDAQ): An example of a company specializing in a diverse portfolio of commercial insurance and reinsurance lines, covering risks such as energy, property, general aviation, construction and engineering, and professional and financial liabilities globally.

-

Firms like AIG (AIG) and The Hartford (HIG) also have significant divisions that cover special risks, including cybersecurity and D&O.

Europe:

-

Beazley (BEZ.L) in the UK is a leading player in specialized insurance, especially in cyber risks.

2.6. Pet Insurers 🐾

Their main purpose is to provide protection for pets, primarily dogs and cats, covering the costs associated with veterinary visits, emergencies, or routine check-ups, thereby mitigating the high expenses that owners may face.

This business model not only facilitates access to affordable veterinary care for pet owners but also benefits veterinarians by attracting more clients to their practices, improving the overall veterinary business.

The range of animal insurance offerings is diverse and extends to various pet-related businesses:

-

Dog Walker Insurance: Includes civil liability and accident and injury coverage.

-

Pet Grooming Insurance: Offers specific coverages for aesthetic care services for animals.

-

Pet Sitter, Boarding, and Doggy Daycare Insurance: May include civil liability, business interruption, and equipment insurance.

-

Dog Trainer and Physiotherapist Insurance: Provides professional coverages tailored to these specialized activities.

-

Microchip Implantation and Pet Transport Insurance: Offers specific protection for these services.

-

Animal Illness Coverage (Vet Fees): Covers medical care costs, which is a significant relief for owners.

United States: Trupanion (TRUP) is a leading pet insurer in North America. There are also other larger insurers that have entered this market or have dedicated divisions, even if it is not their main business.

Europe: Several insurers, including some of the large ones like AXA, offer pet insurance products in European markets.

2.7. Reinsurers 🤝

Reinsurers are companies that operate at a higher level within the insurance value chain: they insure other insurers. Their primary function is to assume a portion of the risks that primary insurance companies (those that sell policies directly to customers) have underwritten, in exchange for a portion of the premiums.

The purpose of reinsurance is multifaceted and crucial for the stability of the sector:

-

Risk Diversification: Allows primary insurers to reduce their exposure to large losses from catastrophic claims or from the accumulation of individual risks. This is vital, for example, when an event like the DANA in Valencia causes massive losses, and a reinsurer like Mapfre RE assumes a fifth of those losses, alleviating the burden on the primary insurer.

-

Results Stabilization: By transferring part of their risks, primary insurers can smooth the volatility of their results, especially in non-life branches, which are more susceptible to large fluctuations in claims.

-

Increased Capacity: Reinsurance allows insurers to underwrite larger or riskier policies than their own capital would permit, thus expanding their business capacity.

Regarding their business models, traditionally there were pure reinsurers, which focused exclusively on reinsurance. However, in recent years, these have become a rarity, as many seek to diversify their portfolio by branching into the primary space. This has led to integrated or diversified reinsurers, which combine reinsurance with direct insurance activities.

The global reinsurance market is highly concentrated, with major reinsurers, such as Munich Re and Swiss Re, dominating a significant market share. These large corporations maintain strong and long-term relationships with brokers and cedents (primary insurers), which gives them considerable pricing power in a market with high barriers to entry.

Reinsurers are particularly sensitive to major natural catastrophes, as they are the entities that ultimately bear a substantial portion of the massive losses generated by these events. This forces them to have sophisticated risk models and maintain high capital levels.

Europe: Munich Re (MUV2.DE) in Germany and Swiss Re (SREN.SW) in Switzerland are the two largest players in the global reinsurance market.

Spain: Mapfre Re, although it is a subsidiary of Mapfre (MAP.MC) and not an independent listed company, is a highly relevant Spanish reinsurer internationally.

3. Financial Analysis of Insurance Companies 📊

3.1. Income Statement (P&L) Specifications for Insurers 📈

The key elements found in these statements include:

3.1.1 Combined Ratio

This indicates the efficiency of the insurance business in Non-Life insurance. It is calculated as:

Combined Ratio = (Claims + Expenses) / Earned Premiums

A ratio of less than 100% indicates that the insurer is profitable from its core business. Conversely, a ratio above 100% indicates that the company is losing money on its primary business and might rely on investment income for profitability.

Example of the Kinsale Capital Group, Inc.

3.2. Balance Sheet Structure Specifications for Insurers ⚖️

The balance sheet structure of an insurance company also has peculiarities that distinguish it from companies in other sectors. The Accounting Plan for Insurance Entities (PCEA) is the framework governing their accounting, structured in five parts including the conceptual framework, recognition and valuation rules, annual accounts, chart of accounts, and accounting definitions.

The key components of an insurer's balance sheet are similar in their general classification to other companies, but with specific emphasis and details:

-

Assets: Divided into non-current assets (such as tangible and intangible fixed assets, and long-term investments) and current assets (such as inventories, trade receivables, and cash).

-

Liabilities: Includes non-current liabilities (interest-bearing loans, deferred taxes, pension commitments) and current liabilities (trade payables, short-term loans, and warranty provisions).

-

Shareholders' Equity: Composed of own funds (originated from shareholder contributions or accumulated earnings), fair value adjustments, and grants or donations received.

However, the most distinctive peculiarities of the insurance balance sheet lie in:

-

Technical Provisions: This is undoubtedly the most significant and characteristic liability of an insurer. They represent the company's future obligations to meet claims and benefits promised to policyholders. Their correct estimation and management are crucial for the company's financial health. They are broken down into several types:

-

Unearned Premium Reserve (UPR): Corresponds to the portion of premiums collected that has not yet been earned, i.e., covering risks that have not yet expired.

-

Provision for Unexpired Risks (PUR): For risks that have already started but have not yet ended.

-

Outstanding Claims Reserve (Claims Not Yet Settled): Intended for claims that have already occurred and been reported but have not yet been paid. It also includes an estimate for claims incurred but not yet reported (IBNR).

-

Mathematical Reserve (Life): Specific to life insurance, it represents the present value of the insurer's future long-term obligations to its policyholders.

-

Catastrophe Reserves: Funds set aside to cope with large-scale, low-probability events such as earthquakes or hurricanes.

-

-

Investments: An insurer's assets are heavily composed of financial investments, which may include fixed income, equities, and real estate. This is because premiums collected are invested until claims are paid, thereby generating additional financial income.

-

Current/Non-Current Classification: In the insurance balance sheet, the distinction between current and non-current assets is often not made in the same way as in other industries. This can make liquidity analysis using traditional ratios difficult. Solvency is analyzed differently, focusing on the minimum capital required by regulation.

3.2.1 Solvency Ratio

Evaluates the insurer's ability to cover its financial obligations:

Solvency Ratio = Available Capital / Required Capital

It should be greater than 100%. If it falls below, the company needs recapitalization or corrective measures.

Technical provisions are at the heart of risk and capital management. Technical provisions stand out as a central and unique component of an insurer's balance sheet, representing "future obligations." This is not just a liability; it is the essence of their business model: managing future payments. The accurate estimation and management of these technical provisions are of utmost importance for an insurer's financial health. Underestimating them can lead to future solvency crises, while overestimating them can unnecessarily tie up capital. For investors, understanding the methodology and prudence behind these provisions is critical. It's a key area where accounting estimates directly impact profitability and risk, making it a qualitative factor to examine alongside quantitative metrics. This also directly links to the concept of "float" discussed earlier, as these provisions represent the funds generated from premiums that are available for investment.

3.3. Different Forms of Income 💰

Insurance companies are, in essence, for-profit businesses that seek to collect more than they pay out in claims and operating expenses. Their business model is based on two main sources of income, which operate in synergy to ensure their profitability and sustainability: underwriting income and investment income.

3.3.1. Underwriting Income:

This is the primary and most direct source of income, derived from the core insurance activity. The majority of this income comes from collecting premiums from policyholders. The determination of these premiums is based on a meticulous analysis of three key factors:

-

The type of insurance coverage

-

The policyholder's risk profile

-

The statistical probability of a claim occurring.

Risk-adjusted pricing allows insurers to maintain their financial stability, covering expected claims, operating costs, and generating profits. Efficient underwriting results in a surplus of premium income over claims payments.

Diligent claims processing, ensuring accuracy and filtering out fraud, is crucial to preserving this income, preventing unjustified payments.

3.3.2. Investment Income:

The composition of the investment portfolio is a critical aspect. Insurers manage the resources entrusted to them by their clients, investing in highly-rated companies and assets. For example, a significant portion of their investments (around 42%) is allocated to government debt securities, and they also hold positions in fixed income and equities.

An interesting concept in the income model is unearned gains. This occurs when policyholders survive term policies or decide not to renew their coverage. In these cases, the risk is transferred back to the consumer, and insurers retain the premiums paid without the obligation to cover future losses, which becomes a gain for the company.

The synergy and counterbalance between underwriting and investment are fundamental. Insurers have two main sources of income: underwriting (premiums) and investments. These are not simply two separate categories but are deeply interconnected, as the "float" generated by premiums drives investment income. The interaction between these two sources is crucial for overall profitability. Strong underwriting performance (a low combined ratio) provides a larger and more stable "float" for investment, which in turn improves financial income.

4. Key Ratios for Evaluating an Insurer

Evaluating an insurance company requires the use of industry-specific metrics that go beyond traditional financial ratios. These indicators provide deep insight into the technical profitability, operational efficiency, and financial strength of the company.

4.1. Combined Ratio 🔗

The combined ratio is a fundamental indicator that measures the technical or operational profitability of Non-Life insurance. It is, in essence, the sum of the loss ratio and the expense ratio, normally calculated on earned premiums net of reinsurance.

Its formula is simple:

Combined Ratio = Loss Ratio + Expense Ratio

The interpretation of this ratio is direct and crucial for investors:

-

If the Combined Ratio is < 100%: Indicates that the insurer is profitable in its underwriting operations. This means that premium income exceeds claims expenses and operating expenses, which is a very positive sign for the company.

-

If the Combined Ratio is > 100%: Suggests that the insurer is experiencing a loss in its underwriting activity, as its expenses (claims and operating) exceed premium income. In this scenario, the company's overall profitability would depend on other income, such as financial income from its investments.

4.2. Loss Ratio 📉

The loss ratio is a key indicator in the insurance sector that measures the proportion between the cost of paid claims and the volume of premiums collected by an insurer. In essence, it indicates the percentage of premiums allocated to paying claims.

The formula for calculating this ratio is:

Loss Ratio = (Cost of Paid Claims / Total Premiums) × 100

The interpretation of the loss ratio is crucial for evaluating profitability and efficiency in risk underwriting:

-

Low (< 70%): May indicate good profitability in the insurance business, as the insurer is paying few claims compared to its income. However, if it is extremely low, it could suggest that premiums are excessive in relation to the assumed risk.

-

Moderate (70%-90%): This range is usually considered ideal, as it allows the insurer to cover claims without compromising its profitability and maintain a good relationship between premiums and risks.

-

High (> 90%): Suggests that the insurer is paying many claims compared to its income. This can affect the company's profitability and is a sign that there might be an imbalance between premiums and insured risk.

4.3. Expense Ratio 💸

The expense ratio is a financial indicator that reflects the percentage of premium income that an insurance entity dedicates to its operating expenses. That is, it measures the efficiency with which the company manages its administrative and acquisition costs.

The formula for calculating this ratio is:

Expense Ratio = (Underwriting Expenses / Earned Premiums) × 100

Where:

-

Underwriting Expenses include costs associated with issuing and operating policies, such as commissions paid to agents and brokers, administrative costs, and other operating expenses.

The interpretation of this ratio is straightforward: a low expense ratio indicates high operational efficiency and effective cost control by the insurer.

The importance of an efficient expense ratio is undeniable for the overall profitability of the insurer, as it directly contributes to maintaining a healthy combined ratio (below 100%). Optimizing this ratio is often achieved through investment in technology, which allows for process automation, reduces the need for manual intervention, and ultimately lowers administrative costs.

4.4. Solvency Ratio ✅

The solvency ratio is a vital financial metric that measures an insurance company's ability to cover its liabilities (including claims and other obligations) with its assets, and to meet its long-term payment obligations. In other words, it indicates whether the company possesses sufficient financial resources to fulfill all its commitments.

The general formula for the solvency ratio is:

Solvency Ratio = Assets / Liabilities

However, in the regulatory context, especially in the European Union, a more specific formula is used:

Solvency Ratio = (Available Capital / Required Capital) × 100

Where Required Capital can take two forms:

-

Solvency Capital Requirement (SCR): Represents the minimum capital level a company must hold to continue its activities without restriction. It is calculated with a 99.5% confidence level over a one-year horizon, implying only a 0.5% probability that losses will exceed this capital in a year.

-

Minimum Capital Requirement (MCR): This is a lower threshold than the SCR, calibrated with an 85% confidence level. If eligible own funds fall below the MCR, the company must communicate urgent measures to the supervisor.

The interpretation of the solvency ratio is crucial for confidence in the insurer:

-

Above 100%: Indicates that the company fully complies with regulatory requirements and that its eligible own funds cover the solvency capital requirement. The higher the ratio above 100%, the stronger the company's balance sheet is considered.

-

Below 100%: Signals financial weakness, implying that own funds are insufficient to cover the required capital, exposing policyholders to a high level of risk.

Sector Example: In Spain, the aggregate solvency ratio for entities stood at an average of 247% in June 2025, with significant dispersion among companies.

The importance of the solvency ratio is paramount. It is a vital metric for evaluating the financial health and long-term stability of an insurer. For consumers, it is a crucial factor when choosing an insurance company, as it gives them peace of mind that their claims will be honored.

5. Valuation of Insurers

When it comes to valuing an insurance company, there are two key financial indicators that allow us to understand both its profitability and its market valuation: Return on Equity (ROE) and the Price-to-Book (P/B) multiple.

5.1 ROE (Return on Equity)

ROE is the fundamental indicator for measuring an insurer's profitability and, in essence, how efficiently it is using its shareholders' capital to generate profits. It is calculated by dividing the company's net profit by its shareholders' equity:

ROE = Net Profit / Shareholders' Equity

A higher ROE generally indicates that the insurer is more effective at managing its capital to produce earnings. It is a crucial barometer for investors looking for companies that maximize the return on their investment.

5.2 Price-to-Book (P/B) Multiple

The Price-to-Book (P/B) multiple is a valuation tool that helps us understand how the market values an insurer in relation to its book equity. It is calculated by dividing the share price by the book value per share:

This multiple is particularly useful because it compares a company's market value with the value of its net assets as they appear on its balance sheet. A P/B greater than 1x suggests that the market values the company above its book value, which could indicate good growth prospects or efficient management. Conversely, a P/B less than 1x might suggest that the market perceives the company to have less value than its book assets.

It is important to note that the interpretation of P/B is often directly related to the insurer's ROE:

-

For insurers with an ROE less than 10%: A more conservative P/B multiple, ranging between 0.6x and 1x book value, is generally applied. This reflects that the market does not expect the company to generate large returns on its equity.

-

For insurers with an ROE of 18-20%: In this case, the market tends to reward high profitability with a significantly higher P/B multiple, which can reach up to 3x book value. This indicates that investors are willing to pay a premium for the insurer's ability to generate high returns.

6. External Factors 🌪️🌊

The insurance sector, by its nature of risk management, is intrinsically vulnerable to a number of external factors. Major natural catastrophes and the constant evolution of regulations are two of the most influential elements that shape insurers' strategy, profitability, and resilience.

The impact of climate change directly manifests in the insurance sector through the increased frequency and severity of natural catastrophes. This phenomenon is continually influencing the behavior of individual events and broader weather patterns, leading to a significant increase in claims costs for insurers.

This increase in claims directly impacts the profitability of insurers. To adapt to the greater exposure to these events, some companies have adjusted their underwriting policies and increased their rates.

7. Regulations 🏛️

Regulation is a constant and highly concerning factor in the insurance sector, holding a prominent position among the main risks. Its impact is profound, shaping operations, strategy, and the very structure of the market.

The main objectives of regulation in the insurance sector are:

-

Consumer Protection: Ensuring that insurance products are accessible, fairly priced, and transparent, protecting policyholders from unfair or illegal practices by insurers.

-

Financial Stability and Solvency: Ensuring that insurance companies operate in a financially stable and solvent manner, maintaining sufficient capital to cover potential losses and risks, and thus fulfilling their long-term obligations.

-

Fair Competition: Promoting a competitive and resilient market, preventing monopolies or practices that harm free competition.

Key regulatory frameworks that exemplify this influence include:

-

Solvency II (European Union): In force since 2016, this directive requires EU insurance and reinsurance companies to hold sufficient financial resources and establishes rigorous rules for governance, risk management, transparency, and supervision. It determines capital requirements based on the risks assumed by the company, such as the Solvency Capital Requirement (SCR) and the Minimum Capital Requirement (MCR).

-

NAIC (National Association of Insurance Commissioners, USA): In the United States, the NAIC is the standard-setting body that provides expertise, data, and analysis to state insurance regulators. Its guidelines and regulations have a significant impact on insurers' operations, consumer protection, and market stability. It establishes Risk-Based Capital (RBC) requirements and guidelines for financial reporting, disclosure requirements, and claims handling.

-

The Centers for Medicare & Medicaid Services (CMS) is the federal agency that administers Medicare and Medicaid, and sets the rules, guidelines, and compliance requirements for healthcare providers and insurers participating in these programs. This includes regulations on eligibility, covered benefits, provider networks, pricing (premiums and co-payments), marketing and enrollment, as well as strict reporting and auditing requirements.

The impact of regulation on operations and strategy is multifaceted:

-

Capital Requirements: Regulations impose significant capital requirements, which affect insurers' ability to invest, expand, or return capital to shareholders.

-

Compliance Costs: The complexity and detail of regulations can lead to high compliance costs, especially for smaller insurers that lack the necessary resources and expertise.

-

Governance and Risk Management: Regulations require robust governance and risk management systems, which implies continuous investments in infrastructure, personnel, and processes.

-

Transparency and Disclosure: Companies are obliged to publicly disclose detailed information about their financial and solvency situation, which increases market transparency.

-

Innovation: To foster innovation without compromising protection, "regulatory sandboxes" may emerge, allowing insurtechs to test new products and services in a controlled environment.

-

Impact on Prices and Products: Market conduct regulation seeks to ensure reasonable rates and access to compliant products, protecting consumers from unfair practices and directly affecting insurers' pricing strategies.

Globally, the trend in regulation points to replacing ex-ante control mechanisms with those that guarantee a dynamic framework, with greater responsibility lying with the insurance entities themselves. The International Association of Insurance Supervisors (IAIS) works on harmonized frameworks for international solvency supervision.