🌱 𝗦𝗸𝗶𝗻 𝗶𝗻 𝘁𝗵𝗲 𝗚𝗮𝗺𝗲 - 𝗧𝗵𝗲 “𝗙𝗼𝘂𝗻𝗱𝗲𝗿 𝗘𝗳𝗳𝗲𝗰𝘁”

Why does money follow its owner?

If you've ever wondered what separates a company that multiplies your money from one that just vegetates in the market, the answer is usually found in the boss's office.

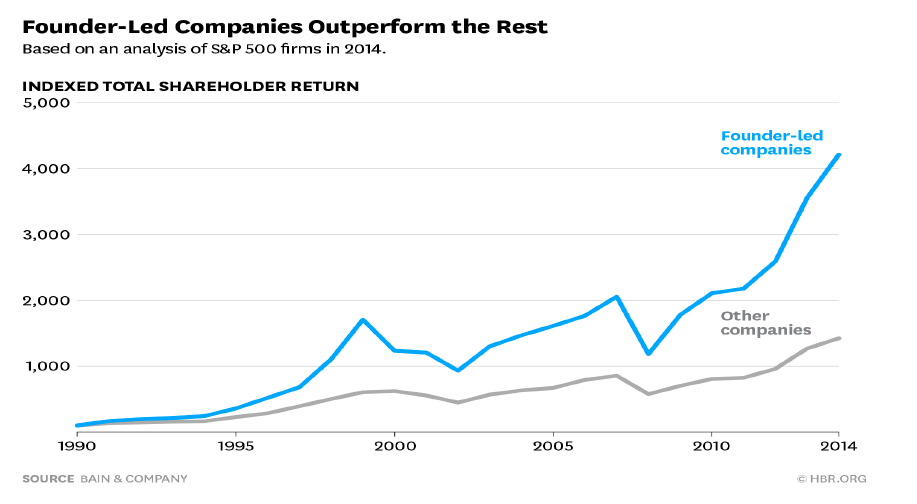

Looking at the Bain & Company chart, the conclusion is a harsh reality check for corporate committee lovers: founder-led companies completely obliterate the performance of the rest of the S&P 500 📈. From 1990 to 2014, the indexed return of companies with their founder at the helm surpassed 4,000 points, while the "other" companies barely scraped 1,400.

Why does this happen? Because of a core investing concept: Skin in the Game 🎯. It's not the same to fly a plane if you own the aircraft and are sitting inside it, compared to being a hired pilot who gets paid the same whether the landing is smooth or sketchy. To understand the backdrop of this chart, we must master the hidden laws that drive the behavior of those at the top.

To understand why the companies in the chart beat the market in such a humiliating fashion, we need to understand what goes on inside a founder's head versus a hired CEO's.

1. The Executive 👔 VS The Shareholder 💼

This is a business school classic. It happens when the interests of the person managing the company (the agent) don't align with those of the person owning the money (the principal, aka you).

-

The Mercenary CEO: His number one priority is usually not screwing up so he doesn't get fired. He wants to maintain his status, his multi-million dollar salary, and secure this year's bonus. If hitting his bonus means earnings per share (EPS) must go up this quarter, he will slash research and development (R&D) without caring if it destroys the company a decade from now. After all, he probably won't even be there anymore.

-

The Founder: Doesn't need to look good in front of a committee every three months. His name is on the door. His net worth and legacy depend on the company becoming a giant 10 or 20 years down the line. If he has to lose money two years in a row to crush the competition with a new product, he will do it without blinking.

2. Capital Allocation 💰

A hired CEO and a founder spend money in radically different ways. Capital allocation is a management team's most critical superpower.

3. Dual-Class Shares: The "Super Vote" Trick 🗳️

Sometimes you'll see companies where the founder only owns 10% of the economic shares but controls 60% of the votes through dual-class shares (Class A, Class B, etc.).

-

The Good Part: It protects the founder from Wall Street's absurd pressures. If generic analysts demand cuts to boost next month's margins, the founder can tell them to take a hike because they have absolute voting control (think Alphabet or Meta).

-

The Bad Part (The Dictatorial Risk): If the founder loses their mind, becomes obsolete, or starts making terrible decisions driven by ego, minority shareholders have zero legal tools to kick them out or redirect the company. You're tied to their genius... or their madness.

4. Succession Risk: The Danger of "The Day After" 🚪

The chart shows us a gold mine, but every mine has its hazards. The biggest risk for these companies is when the founder decides to step down, retires, or passes away.

-

The Cultural Transition: When a founder leaves, the corporate culture usually shifts. The company goes from being a "customer-obsessed startup" to a "process-obsessed, bureaucratic corporation."

-

Real-World Cases: Post-Jobs Apple went from wild disruption to Tim Cook's precision supply chain optimization. Post-Gates Microsoft endured a "lost decade" under Steve Ballmer, focusing on protecting the Windows monopoly instead of spotting the mobile revolution—until Satya Nadella came along to save the day.

5. Ownership %: How Much Should the Founder Own?

To evaluate this in your fundamental analysis, don't just look at a picture of a smiling founder. You need to dive into the Proxy Statement (SEC Form DEF 14A) and check what percentage of shares insiders hold. Here is your level guide:

5.1 🟢 The "Sweet Spot" (The Ideal): Between 5% and 20%

For mid and large-cap companies, this range is pure magic ✨. It's enough skin in the game for the founder to be the most invested person in seeing the stock rise. If the company goes bankrupt, they lose their actual fortune, not just a Christmas bonus.

Note: In mega-caps, 1% or 2% can be perfectly fine if it translates to billions of dollars, like Elon Musk at Tesla or Jeff Bezos at Amazon. The key is that the value of their shares completely dwarfs their salary.

5.2 🔴 Too Much (The "Absolute King" Danger): Over 30% - 40% (In mature companies)

Here, the line between a committed founder and a corporate dictator becomes razor-thin 👑. If the founder controls too many shares or holds super-voting rights, retail shareholders don't mean a thing. If they make terrible choices, the Board of Directors can't fire them. Plus, it reduces the free float, spiking volatility and driving away large institutional funds.

5.3 ⚠️ Too Little (The "Mercenary CEO" Danger): Less than 1% or 2%

Barring mega-corporations, if the management team barely owns any shares in the company they run, sound the alarms 🚨. You're looking at employees in expensive suits who care way more about keeping their jobs. If the stock craters over the long term, they don't care; tomorrow they'll jump to another company with a multi-million dollar golden parachute strapped to their back.

6. Regulation and Insider Trading: The 10b5-1 Plan 🕵️♂️

Now that we know how to measure how many shares the boss holds, we need to track when and how they buy or sell them.

When the founder of a major public company wants to liquidate a block of shares, they don't just pull out their phone, open a trading app, and hit "Sell." If they did that a week before reporting awful earnings, the SEC would handcuff them for insider trading. To avoid prison legally, executives use the 10b5-1 Plan.

6.1 What is this plan and how does it work? 🤖

Think of the 10b5-1 Plan as an automated trading autopilot. The founder goes to an independent broker and says: "Here, set up this order to sell 50,000 shares on the third Tuesday of every quarter for the next two years—I don't care where the market is."

Since the order is scheduled months in advance, if the company tanks the very day after a sale, the founder has an ironclad legal shield: they can prove they didn't execute the order opportunistically; it was automated a long time ago.

6.2 The strict rules of today's game 🛑

Since humans are wired for mischief, executives used to set up these plans and cancel them at will based on whether they knew the quarter was going well or poorly. Regulators got tired of the circus and tightened the rules with clear boundaries:

-

The cooling-off period: When an executive signs or modifies a 10b5-1 Plan, they can't touch a single share right away. They have to wait a minimum of 90 days (or up to two business days after the company reports its financial results for the current quarter). No more setting up a plan on Monday to sell on Friday.

-

No overlapping plans: An executive cannot have multiple 10b5-1 plans open simultaneously with different brokers to hedge their bets or cancel the one that doesn't suit them. Only one active plan is allowed per period.

-

Continuous good faith: The law requires the executive to maintain good faith throughout the entire life of the plan. If they try to manipulate the timing of company news to align with their automated sales, they are in deep trouble.

7. Form 4: Tracking Insider Moves 📋

-

The Form 4: In the US, any insider transaction must be publicly reported on a Form 4 within a maximum of 2 business days. Inside, there is a specific checkbox for the 10b5-1 Plan. If that box is checked, the sale doesn't mean the founder is fleeing a sinking ship; it's simply their automated diversification plan running its course.

Peter Lynch's Golden Rule:

"Insiders might sell their shares for a thousand reasons (buying a mansion, paying for a divorce, or settling taxes)... but they only buy for one reason: they think the price is going up."

If the founder maintains a massive stake and only sells small chunks scheduled via a 10b5-1 Plan, the bullish thesis backing the chart stays fully intact. What you really want to hunt for are direct out-of-pocket buys—the ones executives make with their own cold, hard cash outside of automated plans in the middle of a market crash. That's where you follow the money. 🤑