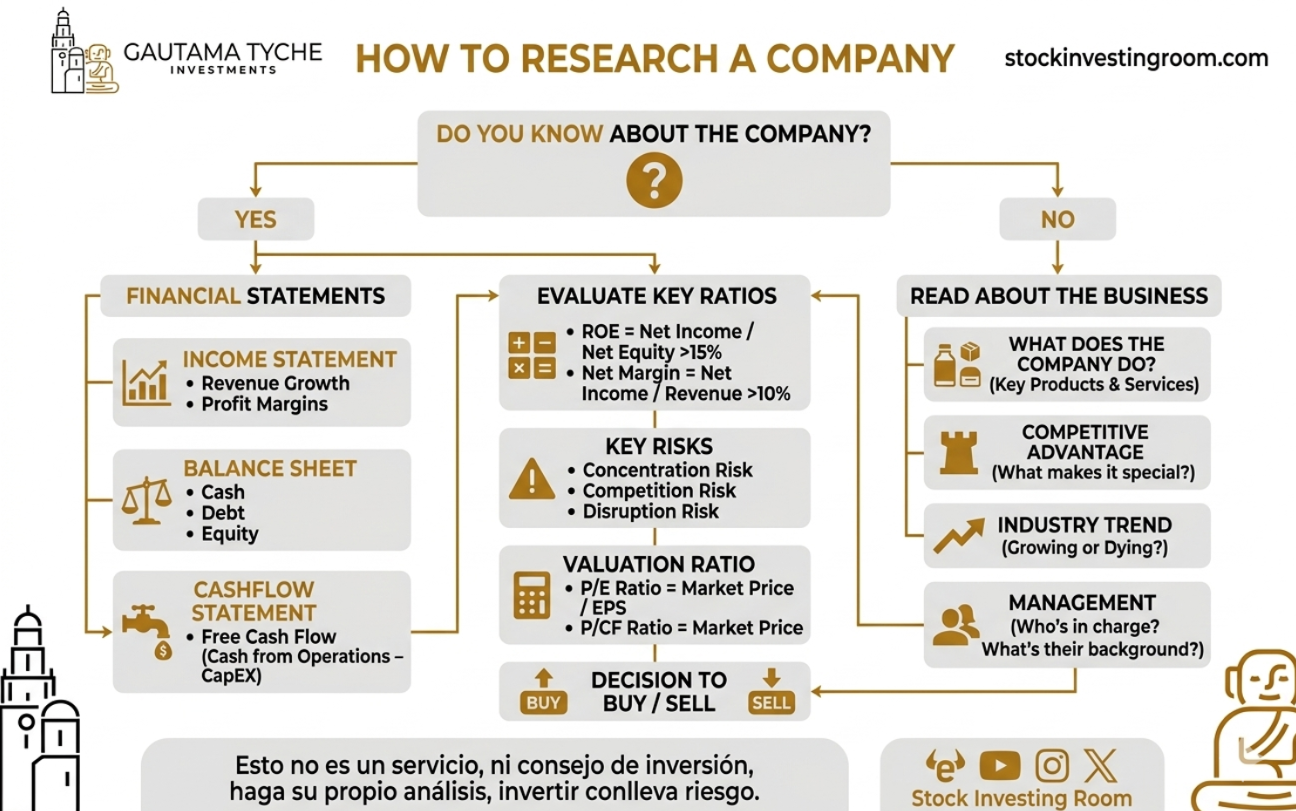

🔎𝗛𝗼𝘄 𝘁𝗼 𝗿𝗲𝘀𝗲𝗮𝗿𝗰𝗵 𝗮 𝗰𝗼𝗺𝗽𝗮𝗻𝘆

Investing isn't just picking a number that goes up and down on an eToro screen while you cross your fingers. If you want to gamble, casinos have much better lighting and usually offer free drinks. In this school, we focus on understanding what is actually behind the ticker. This guide details the logical process to gut a company before putting a single dollar on the line, whether it's trading on the Nasdaq, the Euro Stoxx, or the Hang Seng.

𝟭. 𝗨𝗡𝗗𝗘𝗥𝗦𝗧𝗔𝗡𝗗𝗜𝗡𝗚 𝗧𝗛𝗘 𝗕𝗨𝗦𝗜𝗡𝗘𝗦𝗦 🏗️🏢

Before looking at a single number, you must understand what the company actually does. If you can't explain how the company makes money to your grandmother in two sentences, don't invest.

-

Key Products and Services: Identify what the company really sells. It’s not the same for Apple to sell hardware as it is to sell subscription services with massive margins. In the U.S. market, we usually look for tech leaders; in Europe, we focus more on luxury or consumer staples; and in China, the focus is often on e-commerce platforms and mass services.

-

Competitive Advantage (The Moat): Why don't customers switch to the competition? It could be brand (Coca-Cola), switching costs (Microsoft Windows), or network effects (Alphabet). If a company doesn't have something that makes it special, it’s a commodity, and its fate is to die in a price war.

-

Industry Trends: Is the sector growing or sinking? Investing in typewriter manufacturers in the 90s was a brilliant idea... if you wanted to lose everything. We look for tailwinds, not industries currently in the ICU.

-

Management and "Skin in the Game": Who is at the helm? We look for managers with an impeccable track record and, above all, who own shares in their own company. If the CEO is selling their stock while telling you everything is great, run. It’s like a chef who refuses to taste their own cooking.

𝟮. 𝗧𝗛𝗘 𝗧𝗛𝗥𝗘𝗘 𝗙𝗜𝗡𝗔𝗡𝗖𝗜𝗔𝗟 𝗦𝗧𝗔𝗧𝗘𝗠𝗘𝗡𝗧𝗦 📊📑

Once we like the business, let's see if the numbers back up the story. Numbers don't lie, though accountants sometimes like to "apply a bit of makeup."

2.1 The Income Statement (The Performance Snapshot)

Here we look at whether the company sells more every year (Revenue Growth) and what part of those sales stays in the pocket after paying expenses (Profit Margins). If revenue is up but profits are down, the company is working for everyone else except you.

2.2 The Balance Sheet (The Health Check)

This is the medical exam. We look at three things:

-

Cash: Do they have enough money in the bank to survive a crisis?

-

Debt: A company with too much debt is a house of cards. In Europe, companies tend to be more conservative with debt, whereas in the U.S., leverage is more common to accelerate growth.

-

Equity: What’s left if they sold everything and paid everyone off tomorrow. We want this value to grow over time.

2.3 The Cash Flow Statement (The Naked Truth)

Net profit can be manipulated with accounting tricks, but the money flowing in and out of the bank is sacred. The key metric here is Free Cash Flow (FCF).

-

Formula:

$$Free Cash Flow = Cash from Operations - CapEX$$This is the actual cash left to pay dividends, buy back shares, or keep growing without having to beg for a loan.

𝟯. 𝗘𝗩𝗔𝗟𝗨𝗔𝗧𝗜𝗡𝗚 𝗞𝗘𝗬 𝗥𝗔𝗧𝗜𝗢𝗦 𝗔𝗡𝗗 𝗥𝗜𝗦𝗞𝗦 ⚖️⚠️

Not all companies are created equal. To separate the wheat from the chaff, we use quality filters.

-

ROE (Return on Equity): Should be above 15%. This indicates how efficient management is at using shareholders' money to generate more money. A low ROE is usually a symptom of mediocre management or an unprofitable business.

-

Net Margin: Should be above 10%. If a company earns less than 10 cents for every dollar it sells, any small supply chain issue or tax hike will put them in the red.

-

Concentration and Disruption Risks: Does the company depend on a single client (like many Apple suppliers)? Is there a new technology that will make their product obsolete? In China, for example, political risk is a concentration factor you cannot ignore; one regulatory change and your investment evaporates.

𝟰. 𝗩𝗔𝗟𝗨𝗔𝗧𝗜𝗢𝗡: 𝗜𝗦 𝗜𝗧 𝗖𝗛𝗘𝗔𝗣 𝗢𝗥 𝗘𝗫𝗣𝗘𝗡𝗦𝗜𝗩𝗘? 🏷️💰

Even the best company in the world is a bad investment if you pay too much for it. Buying Nvidia at any price just because "it's the future" is the fastest way to see your portfolio in the red for years if the valuation doesn't match the reality.

-

P/E Ratio (Price-to-Earnings): Tells us how many years it would take to recover our investment via profits. A P/E of 50 means you are paying for 50 years of current earnings. Unless you expect the company to grow like wildfire, it’s a red flag.

-

P/FCF Ratio (Price-to-Free Cash Flow): More reliable than the P/E because it’s based on real cash. We look for companies trading at reasonable multiples relative to the cash they actually generate.

𝟱. 𝗗𝗘𝗖𝗜𝗦𝗜𝗢𝗡 𝗠𝗔𝗞𝗜𝗡𝗚 🏁🛠️

After this analysis, there are only two paths:

-

BUY: If you understand the business, the numbers are solid, risks are manageable, and the price is fair or cheap.

-

SELL / PASS: If the business is confusing, the debt is scary, or the valuation is simply in the stratosphere due to pure market hype.

Successful investing doesn't require being a math genius; it requires the discipline to follow this process and not get swept away by FOMO (Fear Of Missing Out). If you do your homework, the stock market will stop looking like a casino and start looking like a serious business.