𝗜𝗻𝘃𝗲𝘀𝘁𝗺𝗲𝗻𝘁 𝗙𝘂𝗻𝗱𝘀 𝗮𝗻𝗱 𝗘𝗧𝗙𝘀

1. Traditional Mutual Funds 🏦

A mutual fund is like a collective basket where many investors pool their money together. A team of professionals is in charge of moving that capital to buy assets (stocks, bonds, etc.) based on the fund's strategy.

Depending on what they invest in and how they are managed, we find these main types:

- 📈 Equity Funds (Active Management): They invest mainly in company stocks. Here, managers try to "beat the market" by stock-picking what they think will go up. The perfect historical example is Peter Lynch, who managed the Magellan Fund and achieved a spectacular 29% average annual return between 1977 and 1990.

- 📉 Fixed Income Funds (Active Management): They buy debt (government or corporate bonds). Managers look to scrape together the maximum return by closely watching interest rates and default risks.

- ⚖️ Balanced / Mixed Funds (Active Management): A mix of the two previous types to balance risk. The classic example is the 60/40 portfolio (60% stocks, 40% bonds), which shifts depending on the manager's moves.

🔄 What happens to the profits? Accumulation vs. Distribution

-

Accumulation funds: If the companies in the basket pay dividends, the fund automatically reinvests them to buy more shares. This makes your money grow faster thanks to compound interest. It is the ideal option to grow your wealth.

-

Distribution funds: Dividends or interest are paid directly into your checking account on a regular basis. Useful if you already live off your investments and need cash month by month.

2. The Acronym Labyrinth: ETP, ETF, ETN, and ETC 🌐

This is where people usually get massively confused. The financial industry uses the word ETP as an umbrella term that hides different exchange-traded products. Let’s crack the code:

📦 ETP (Exchange Traded Product): This is the generic term. It simply means "Exchange Traded Product". If it trades on the market just like a stock, it’s an ETP. Within this big family, we find the following three.

- 📊 ETF (Exchange Traded Fund): This is an exchange-traded fund. Its goal is usually to track an entire index (like the S&P 500) or a specific sector (semiconductors, cybersecurity, defense, health). When you buy a share, you own a proportional part of all the stocks that make up that index. They are physically backed by the assets they buy.

- 🛢️ ETC (Exchange Traded Commodity): These are exchange-traded products specialized in commodities (gold, oil, gas, wheat...). Instead of buying a physical gold bar or a crude oil barrel and putting it in your storage room, you buy an ETC that mirrors its price. Some are physically backed (they have the gold locked in a vault) and others use financial contracts.

- ⚠️ ETN (Exchange Traded Note): Careful with these. They are not funds; they are debt securities (bank notes) issued by a financial institution to replicate an index or an exotic asset. The real danger here is the "counterparty risk": if the bank that issued the ETN goes bankrupt, you are left with nothing, as there are no physical shares backing your money, just the bank's promise to pay.

3. How do ETFs work and where to find them? 🛒

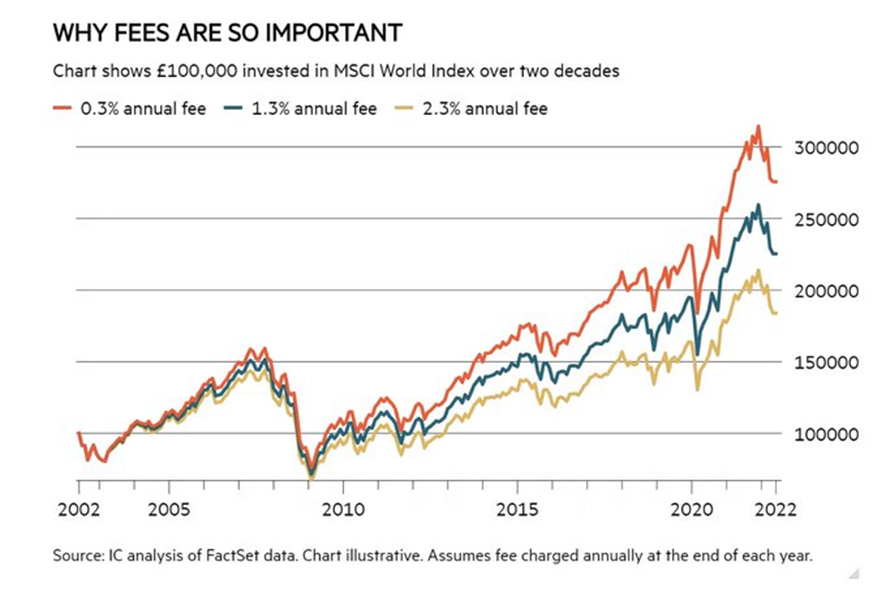

Unlike traditional mutual funds, which only calculate their price once a day when the market closes, ETFs are bought and sold in real-time during market hours, exactly like an Apple or Telefónica stock. They have two massive advantages: they are extremely transparent and their fees are ridiculously low (usually ranging between 0.1% and 0.9%, reaching 1.5% at the absolute most). In contrast, traditional active management can crush you with cumulative fees between 3% and 15% if you add up management, subscription, redemption, or performance fees.

To build your portfolio with these assets, you have two paths:

-

Manual Option: You open an account with a broker yourself, search for the ETFs you want, and buy them according to your strategy.

-

Automated Option (Robo-Advisor): An automated manager gives you a risk profile test and designs an ETF portfolio for you, rebalancing the money automatically without you having to lift a finger.

🔍 Essential pages to search and compare ETFs:

-

JustETF (Excellent for European investors)

-

ETFdb (A colossal database)

-

ETF.com (In-depth analysis)

4. Great Debate: Active vs. Passive Management 🥊

To decide where to put your savings, you need to understand the rules of the game for each side:

🧠 Active Management (Traditional Funds)

-

The promise: A star manager is going to study the market to dodge the hits and find the best opportunities to beat the benchmark index.

-

The harsh reality: Very few manage to do it in the long run. Plus, the drag of high fees makes it very difficult to come out on top. Their big advantage is the flexibility to hold liquidity (cash) if they see a market crash coming.

🤖 Passive Management (ETFs and Index Funds)

-

The promise: We don't try to be smarter than anyone else. If the S&P 500 goes up, your portfolio goes up; if the S&P 500 goes down, your portfolio goes down. You replicate the exact market.

-

The big advantage: Since they don't need an army of analysts collecting millionaire bonuses, costs are minimal. Those fee savings stay in your pocket and, in the long run, make a massive difference in your portfolio's final return. The downside is that if the market takes a dive, you take the full hit without anesthesia.

In the end, the key for any retail investor comes down to diversifying, keeping costs as low as possible, and letting time do its magic.