🌐The Economic Cycle and Sector Rotation🔄

🌐 T𝗵𝗲𝗼𝗿𝘆 𝗼𝗳 I𝗻𝘃𝗲𝘀𝘁𝗺𝗲𝗻𝘁 C𝘆𝗰𝗹𝗲𝘀 𝗳𝗼𝗿 P𝗿𝗼𝗳𝗲𝘀𝘀𝗶𝗼𝗻𝗮𝗹𝘀 📈

A deep understanding of the economic cycle isn't just an academic exercise; it’s the gravity that pulls every successful investment decision. For an elite investment school, this is the core of profitability. Financial markets don't just move randomly. They follow a wave-like pattern of expansion and contraction. While the timing is never exactly the same, the structure remains solid and predictable throughout history. This dynamic comes from the constant tug-of-war between goods production, household spending, business investment, and the policies of governments and central banks.

For an investor, the economic cycle is the fluctuation of overall activity, mostly seen in Gross Domestic Product ($GDP$). However, it stands on three critical pillars: the corporate earnings cycle, the credit cycle, and the inventory cycle. Mastering these concepts lets a pro spot market turns before they become obvious to everyone else—that’s the real "secret sauce" in portfolio management. In a globalized world, this analysis must look abroad, seeing how powerhouses like the U.S., Europe, and China interact, often while being in completely different phases of their own cycles.

🔄 C𝗮𝗽𝗶𝘁𝗮𝗹 D𝘆𝗻𝗮𝗺𝗶𝗰𝘀 𝗮𝗻𝗱 W𝗲𝗮𝗹𝘁𝗵 C𝗿𝗲𝗮𝘁𝗶𝗼𝗻 💰

The capital cycle, unlike the purely economic one, focuses on how investment flows hit industry profits at a micro level. When an industry shows high returns, it attracts a flood of new money. This over-investment leads to oversupply, which eventually kills profit margins. This triggers a phase of contraction and consolidation, famously known as Schumpeter’s "creative destruction." A top-tier investor must learn to identify not just the global macro phase, but which specific sectors are suffering from a lack of capital or, conversely, are dangerously bloated with over-investment.

| Flow Component | Impact on the Cycle | Consequence for the Investor |

| Household Income | Main source of demand and savings. | Defines the potential of consumer sectors. |

| Business Investment | The engine of productivity and jobs. | Drives industrial and tech sectors. |

| Public Spending | A tool for stabilization or stimulus. | Affects interest rates and overall liquidity. |

| Foreign Sector | Reflects competitiveness and trade. | Determines currency strength and export value. |

📊 𝗠𝗮𝗰𝗿𝗼𝗲𝗰𝗼𝗻𝗼𝗺𝗶𝗰 𝗜𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿𝘀:

🔦 𝗟𝗲𝗮𝗱𝗶𝗻𝗴 𝗜𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿𝘀

These indicators change before the overall economy does, acting as trend detectors. In the context of 2026, the relevance of this data is at its peak to predict whether a slowdown will turn into a deep recession or a soft landing.

- Stock Market Performance: The stock market is the leading indicator par excellence, as it reflects profit expectations six to nine months in advance. A persistent bull market usually precedes $GDP$ expansion, while a prolonged drop warns of economic clouds ahead.

- Building Permits: Given that housing is one of the sectors most sensitive to interest rates, an increase in building permits is an unmistakable sign of future recovery and job creation in related industries.

- Consumer Confidence and Purchasing Managers' Indices (PMI): These reflect spending and production intentions. Levels above 50 in the manufacturing PMI indicate expansion, while drops below this threshold suggest an imminent contraction.

- Yield Curve: An inverted yield curve (when short-term rates exceed long-term ones) is a historically near-infallible predictor of recessions, reflecting that investors expect economic weakness that will force rates down in the future.

⏱️ 𝗖𝗼𝗶𝗻𝗰𝗶𝗱𝗲𝗻𝘁 𝗮𝗻𝗱 𝗟𝗮𝗴𝗴𝗶𝗻𝗴 𝗜𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿𝘀

Coincident indicators, such as $GDP$ and industrial production, confirm the current phase of the cycle we are in. However, it is the lagging indicators that often cause the most confusion for rookie investors. The unemployment rate and inflation usually react months after the economic trend has already changed. For example, in the early stages of a recession, inflation may continue to rise due to price inertia in services, which can lead to monetary policy errors if other data is ignored.

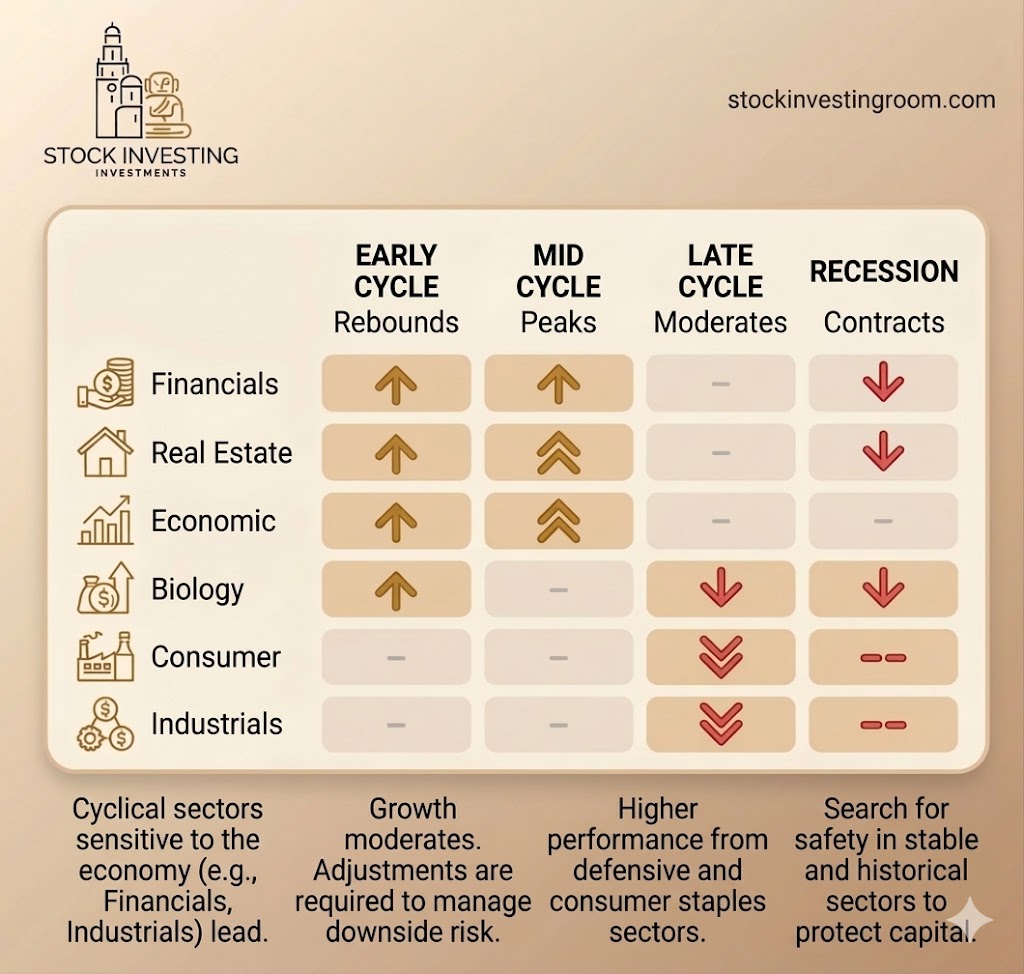

🌱 𝗣𝗵𝗮𝘀𝗲 𝟭: 𝗘𝗮𝗿𝗹𝘆 𝗖𝘆𝗰𝗹𝗲 𝗮𝗻𝗱 𝗥𝗲𝗯𝗼𝘂𝗻𝗱𝘀

The start of the cycle, or early recovery phase, represents the rebirth of economic activity after hitting rock bottom in a recession. This phase is characterized by a shift in sentiment: from extreme pessimism to cautious hope. Macroeconomically, $GDP$ moves from negative to positive rates, and industrial production begins its climb.

🏦 𝗦𝗲𝗻𝘀𝗶𝘁𝗶𝘃𝗲 𝗦𝗲𝗰𝘁𝗼𝗿 𝗟𝗲𝗮𝗱𝗲𝗿𝘀𝗵𝗶𝗽: 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹𝘀 𝗮𝗻𝗱 𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝗶𝗮𝗹𝘀

In this stage, the sectors that suffered the most during the contraction typically lead the returns. The financial sector benefits from a yield curve that starts to steepen and an improvement in credit quality, as defaults begin to decrease. Industrial companies, for their part, experience an increase in orders as economic inventories hit rock bottom and sales start to pick up.

| Sector | Behavior at Start | Fundamental Reason |

| Financials | Significant Rise ↑ | Credit improvement and margin expansion. |

| Real Estate | Recovery ↑ | Low interest rates incentivize buying. |

| Industrials | Activity Rebound ↑ | Inventory restocking and logistics. |

| Economic (General) | Initial Growth ↑ | Public and private investment reactivates. |

| Biology (Health/Biotech) | Moderate Growth ↑ | Investment in innovation resumes with risk appetite. |

🏘️ 𝗥𝗲𝗮𝗹 𝗘𝘀𝘁𝗮𝘁𝗲 𝗮𝘀 𝗮 𝗥𝗲𝗰𝗼𝘃𝗲𝗿𝘆 𝗘𝗻𝗴𝗶𝗻𝗲

The real estate sector is typically the first major engine to fire up. In the United States, interest rate cuts by the Federal Reserve during the previous recession make mortgages cheaper, creating pent-up demand that explodes at the start of the cycle. In Europe, this process can be slower due to market fragmentation, but it follows a similar logic driven by infrastructure funds and fiscal support. It is an ideal time for investors in real assets, as property prices are usually at attractive levels after the adjustment.

🌳 𝗣𝗵𝗮𝘀𝗲 𝟮: 𝗠𝗶𝗱-𝗖𝘆𝗰𝗹𝗲 𝗮𝗻𝗱 𝗖𝗼𝗻𝘀𝗼𝗹𝗶𝗱𝗮𝘁𝗶𝗼𝗻

The mid-phase is traditionally the longest part of the economic cycle. The economy is no longer just bouncing back; it enters a self-sustained and widespread expansion. Growth moderates compared to the explosive start, but it becomes more stable and predictable.

🚀 𝗧𝗵𝗲 𝗣𝗲𝗮𝗸 𝗼𝗳 𝗥𝗲𝗮𝗹 𝗘𝘀𝘁𝗮𝘁𝗲 𝗮𝗻d 𝗘𝗰𝗼𝗻𝗼𝗺𝗶𝗰 𝗚𝗿𝗼𝘄𝘁𝗵 📈

During this phase, the real estate sector reaches its point of maximum frenzy. Consumer confidence is high, unemployment has dropped to historic lows, and access to credit is abundant. It is at this point that the accompanying image indicates "Double Up" growth (⬆️⬆️) for both Real Estate and general Economic performance. Companies invest heavily in fixed capital ($CAPEX$) to satisfy a demand that seems inexhaustible.

-

Credit Dynamics: In the mid-phase, credit growth is strong and healthy. Central banks usually adopt a neutral stance, allowing the economy to grow without intervening aggressively with rate hikes just yet.

-

Consumption and Technology: Discretionary consumption (travel, tech, leisure) shines, as households have excess savings and rising wages. Tech companies benefit from the need for efficiency and automation that arises in an economy operating near full capacity.

⚖️ 𝗥𝗶𝘀𝗸 𝗠𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁 𝗔𝗱𝗷𝘂𝘀𝘁𝗺𝗲𝗻𝘁𝘀 𝗮𝘁 𝘁𝗵𝗲 𝗣𝗲𝗮𝗸

Despite the optimism, the professional investor must start making adjustments to manage downside risk. As we approach the end of the mid-phase, valuation multiples are typically high, and any disappointment in earnings can trigger severe corrections. The right strategy at this point is portfolio rebalancing, ensuring that gains from the most volatile sectors don't leave the portfolio overexposed to a sudden turn in the cycle.

🍂 𝗣𝗵𝗮𝘀𝗲 𝟯: 𝗟𝗮𝘁𝗲 𝗖𝘆𝗰𝗹𝗲 𝗮𝗻𝗱 𝗚𝗿𝗼𝘄𝘁𝗵 𝗠𝗼𝗱𝗲𝗿𝗮𝘁𝗶𝗼𝗻

The end of the cycle is a stage of overheating. The economy begins to hit its capacity limits. Inflation becomes the primary concern for policymakers, triggering interest rate hikes that make the cost of debt more expensive.

🛡️ 𝗥𝗼𝘁𝗮𝘁𝗶𝗼𝗻 𝘁𝗼 𝗗𝗲𝗳𝗲𝗻𝘀𝗶𝘃𝗲 𝗮𝗻𝗱 𝗖𝗼𝗻𝘀𝘂𝗺𝗲𝗿 𝗦𝘁𝗮𝗽𝗹𝗲𝘀 𝗦𝗲𝗰𝘁𝗼𝗿𝘀

As growth weakens toward its stalling speed, investors flee cyclical sectors and seek refuge in stability. This is where sectors like Consumer Staples and more mature Industrials show greater resilience. According to the visual guide, the Consumer and Industrial sectors usually experience a moderation or contraction in their momentum (⬇️⬇️), reflecting that elastic demand is starting to vanish.

| Category | Late Phase Trend | Market Dynamics |

| Biology (Health) | Moderate Decline ↓ | Pressure on margins due to costs, but stable demand. |

| Consumer Staples | Resilience / Stability | Refuge in products for primary needs. |

| Industrials | Decline ↓ | Drop in new orders and accumulation of inventories. |

| Energy | Potential Rise | Often the last sector to fall due to commodity prices. |

🧬 𝗧𝗵𝗲 𝗕𝗶𝗼𝗹𝗼𝗴𝘆 𝗮𝗻𝗱 𝗛𝗲𝗮𝗹𝘁𝗵 𝗦𝗲𝗰𝘁𝗼𝗿 𝗶𝗻 𝗧𝗿𝗮𝗻𝘀𝗶𝘁𝗶𝗼𝗻 🧪

The health sector (represented as Biology) shows complex behavior. Although it is defensive—because people don't stop getting sick—smaller biotech companies that depend on external financing can suffer from credit tightening. However, big pharma offers attractive dividends and secure cash flows that protect them from the general decline. In 2026, biotechnology will also be influenced by its role in national security and defense, which can provide stable government contracts that act as cyclical buffers.

❄️ 𝗣𝗵𝗮𝘀𝗲 𝟰: 𝗥𝗲𝗰𝗲𝘀𝘀𝗶𝗼𝗻 𝗮𝗻𝗱 𝗖𝗼𝗻𝘁𝗿𝗮𝗰𝘁𝗶𝗼𝗻 𝗼𝗳 𝗔𝗰𝘁𝗶𝘃𝗶𝘁𝘆 📉

Recession is the most feared but necessary phase to clean up system excesses. It is characterized by a persistent drop in $GDP$, rising unemployment, and a severe contraction in corporate profits. Credit, the engine of previous phases, dries up, making debt refinancing difficult.

📉 𝗧𝗵𝗲 𝗖𝗼𝗹𝗹𝗮𝗽𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗮𝗻𝗱 𝗥𝗲𝗮𝗹 𝗘𝘀𝘁𝗮𝘁𝗲 𝗦𝗲𝗰𝘁𝗼𝗿𝘀 🏠

In this stage, the accompanying image shows a clear downward trend (⬇️) for the Financial, Real Estate, and Biology sectors. The financial sector suffers from increased delinquency and falling demand for new loans. The real estate sector enters a price adjustment phase, as high interest rates from the end of the previous cycle have killed affordability. In this environment, the investor must prioritize capital protection and liquidity.

-

Search for Safety: Investors take refuge in historical and stable sectors to protect capital. Treasury bonds are usually the star asset, as their price rises when central banks cut interest rates to stimulate the economy.

-

Opportunities at the Bottom: Although recession is painful, it is the moment when the seeds of the next great fortune are sown. Shrewd investors (Smart Money) monitor the market looking for high-quality assets that have been sold indiscriminately out of panic.

💳 𝗧𝗵𝗲 𝗗𝗲𝗹𝗲𝘃𝗲𝗿𝗮𝗴𝗶𝗻𝗴 𝗣𝗿𝗼𝗰𝗲𝘀𝘀 𝗮𝗻𝗱 𝘁𝗵𝗲 𝗗𝗲𝗯𝘁 𝗖𝗿𝗶𝘀𝗶𝘀 🏦

During a recession, the economy must face its debt burden. If debt levels are too high, lowering interest rates might not be enough to jumpstart the economy, leading us into a deleveraging process. In this scenario, companies and households must cut spending to pay off debts, which reduces the system's total income, creating a deflationary vicious cycle. An investment school should teach its students to distinguish between a normal recession and a balance sheet crisis, where deleveraging can last a decade, as seen in certain historical periods in the United States or Japan.

🎢 𝗘𝗺𝗼𝘁𝗶𝗼𝗻𝘀 𝗮𝘀 𝗮 𝗖𝗼𝗻𝘁𝗿𝗮𝗿𝗶𝗮𝗻 𝗜𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿 🧠

The emotional cycle usually runs parallel to the economic cycle but with more pronounced extremes.

-

Euphoria Phase: Coincides with the cycle's peak. It is the point of maximum financial risk, where investors underestimate threats and leverage is at its highest.

-

Panic Phase: Occurs during a deep recession. It is the point of maximum financial opportunity, where assets are sold below their intrinsic value due to irrational fear.

-

Emotional Resilience: The professional investor must develop the ability to act against their primal instincts, buying when there is "blood in the streets" and selling when optimism is universal.

🛡️ 𝗦𝘂𝗿𝘃𝗶𝘃𝗮𝗹 𝗮𝗻𝗱 𝗚𝗿𝗼𝘄𝘁𝗵 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗲𝘀 🚀

It is not enough to have different assets; you must have assets that move in opposite directions. Gold and Treasury bonds usually act as insurance against stock market panic.

| Risk Strategy | Main Objective | Key Tool |

| Diversification | Reduce non-systematic risk. | Sectoral and geographic ETFs. |

| Position Sizing | Avoid bankruptcy from a single error. | Exposure limit per issuer (5-10%). |

| Continuous Monitoring | Adapt to cycle changes. | Analysis of leading indicators ($LEI$). |