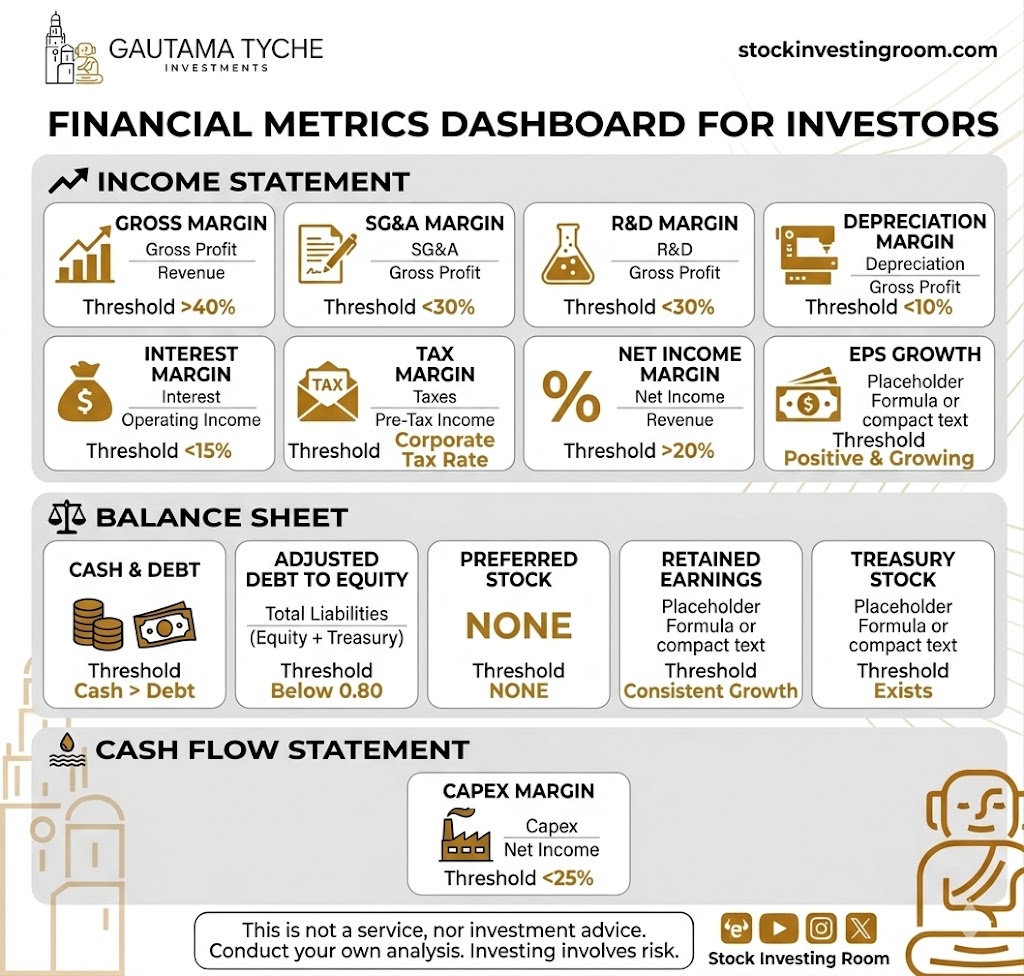

📊 𝗞𝗲𝘆 𝗳𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗺𝗲𝘁𝗿𝗶𝗰𝘀

📈𝟭: 𝗧𝗵𝗲 𝗜𝗻𝗰𝗼𝗺𝗲 𝗦𝘁𝗮𝘁𝗲𝗺𝗲𝗻𝘁

The first place we look is the income statement. This is where the company tells us how much it sells and, more importantly, how much of that actually stays in its pocket after the party is over.

1.1 𝗚𝗿𝗼𝘀𝘀 𝗠𝗮𝗿𝗴𝗶𝗻: 𝗧𝗵𝗲 𝗙𝗶𝗿𝘀𝘁 𝗟𝗶𝗻𝗲 𝗼𝗳 𝗗𝗲𝗳𝗲𝗻𝘀𝗲 🛡️

Gross margin is the percentage of revenue left after deducting the direct costs of producing the goods or services. A threshold above 40% is our smoke signal.

If a company has a high gross margin, it means it has a product people actually want and are willing to pay a premium for. If the margin is low, the company is in a price war with its competition, and in wars, everyone ends up bleeding. We look for companies that sell perceived "quality," not those begging for a penny of profit.

1.2 𝗦𝗲𝗹𝗹𝗶𝗻𝗴, 𝗚𝗲𝗻𝗲𝗿𝗮𝗹, 𝗮𝗻𝗱 𝗔𝗱𝗺𝗶𝗻𝗶𝘀𝘁𝗿𝗮𝘁𝗶𝘃𝗲 𝗘𝘅𝗽𝗲𝗻𝘀𝗲𝘀 (𝗦𝗚&𝗔) 📂

This is where we see if the management is frugal or if they have a taste for unnecessary luxury. SG&A expenses below 30% of gross profit indicate efficiency. If a company spends too much on marketing or internal bureaucracy just to sell the same amount, the product isn't selling itself. Operational efficiency is the difference between a company that creates wealth and one that just moves money from one side to the other.

1.3 𝗥&𝗗 𝗮𝗻𝗱 𝗗𝗲𝗽𝗿𝗲𝗰𝗶𝗮𝘁𝗶𝗼𝗻: 𝗧𝗵𝗲 𝗜𝗻𝗻𝗼𝘃𝗮𝘁𝗶𝗼𝗻 𝗧𝗮x 🧪

Investing in research (R&D) is great, but if a company has to spend more than 30% of its gross profit just to avoid becoming obsolete, you have a problem: you're on a treadmill that never stops. The same goes for depreciation; if it exceeds 10% of gross profit, the company needs to buy new machinery constantly just to keep functioning. We prefer businesses that don't need to reinvent the wheel every Monday.

1.4 𝗡𝗲𝘁 𝗠𝗮𝗿𝗴𝗶𝗻 𝗮𝗻𝗱 𝗘𝗣𝗦 𝗚𝗿𝗼𝘄𝘁𝗵 💰

At the end of the day, net profit is what counts. A threshold above 20% tells us we are looking at a money-making machine. But a static photo isn't enough; we want to see that Earnings Per Share (EPS) is positive and growing. If the company earns more and more for every share you own, your investment will grow naturally without you having to pray for the market to go crazy.

⚖️𝟮: 𝗧𝗵𝗲 𝗕𝗮𝗹𝗮𝗻𝗰𝗲 𝗦𝗵𝗲𝗲𝘁: 𝗦𝘁𝗿𝗲𝗻𝗴𝘁𝗵 𝗮𝗻𝗱 𝗦𝘂𝗿𝘃𝗶𝘃𝗮𝗹

If the income statement is the car's speed, the balance sheet is the chassis. If the chassis is made of paper, the first pothole will ruin the car.

2.1 𝗖𝗮𝘀𝗵 𝗮𝗻𝗱 𝗗𝗲𝗯𝘁: 𝗪𝗵𝗼’𝘀 𝘁𝗵𝗲 𝗕𝗼𝘀𝘀? 🏦

The rule is simple: cash must be greater than debt. A company with a mountain of cash and little debt is the master of its own destiny. It can buy out struggling competitors, buy back its own shares, or simply sleep soundly. A heavily indebted company works for the bank, not for you.

2.2 𝗗𝗲𝗯𝘁 𝘁𝗼 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗘𝗾𝘂𝗶𝘁𝘆 📉

We look for a threshold below 0.80. This measures how much of what the company owns has been financed by the owners versus lenders. A low ratio indicates the company is financially independent. We don’t want partners who owe their shirts; we want companies that finance themselves through their own success.

2.3 𝗣𝗿𝗲𝗳𝗲𝗿𝗿𝗲𝗱 𝗦𝘁𝗼𝗰𝗸 𝗮𝗻𝗱 𝗥𝗲𝘁𝗮𝗶𝗻𝗲𝗱 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 📑

Preferred stock is like an annoying guest who eats before you do; that’s why we look for companies that have noneNONE. We want to be first in line to get paid.

As for retained earnings, we look for consistent growth. If the company saves money year after year and that pile grows, it means the intrinsic value of the business is increasing. That’s compound interest working in the shadows.

2.4 𝗧𝗿𝗲𝗮𝘀𝘂𝗿𝘆 𝗦𝘁𝗼𝗰𝗸: 𝗔 𝗩𝗼𝘁𝗲 𝗼𝗳 𝗖𝗼𝗻𝗳𝗶𝗱𝗲𝗻𝗰𝗲 🗳️

When a company repurchases its own shares and keeps them in treasury, it’s saying: "There is no better investment than ourselves." Furthermore, this reduces the number of shares in circulation, making your slice of the pie bigger without you having to spend an extra cent. We want treasury stock to exist.

🏭𝟯: 𝗧𝗵𝗲 𝗖𝗮𝘀𝗵 𝗙𝗹𝗼𝘄: 𝗥𝗲𝗮𝗹𝗶𝘁𝘆 𝗪𝗶𝘁𝗵𝗼𝘂𝘁 𝗠𝗮𝗸𝗲𝘂𝗽

Accounting can be creative, but cash in the bank doesn't lie. This is where mediocre businesses are separated from the cash cows.

3.1 𝗖𝗔𝗣𝗘𝘅 𝗠𝗮𝗿𝗴𝗶𝗻: 𝗠𝗮𝗶𝗻𝘁𝗲𝗻𝗮𝗻𝗰𝗲 𝘃𝘀. 𝗚𝗿𝗼𝘄𝘁𝗵 🚜

CAPEX (Capital Expenditure) is the money the company spends on physical assets. We want this spending to be below 25% of net profit.

If a company has to spend almost everything it earns fixing factories or buying trucks, there’s nothing left for the shareholders. The best businesses are "asset-light": those that can double their sales without having to double their factories. Fewer bricks and more profits; that’s the key.

🧠𝟰: 𝗜𝗻𝘃𝗲𝘀𝘁𝗺𝗲𝗻𝘁 𝗣𝗵𝗶𝗹𝗼𝘀𝗼𝗽𝗵𝘆 𝗖𝗼𝗻𝗰𝗹𝘂𝘀𝗶𝗼𝗻

This methodology isn't about guessing which stock will go up tomorrow. It’s about identifying companies with a dominant position, smart management, and a financial structure that makes them virtually indestructible.

By filtering through these thresholds, we eliminate the noise and empty promises. We don’t invest in hope; we invest in metrics that prove a company has a durable competitive advantage. If the numbers meet these criteria, the stock price will eventually reflect the quality of the business. Investing this way requires patience and discipline, but it’s the only way to avoid becoming shark bait in the market.