Introduction to investment

Why Should Average People Invest in the Stock Market Instead of Relying on State Pension Plans?

The financial world may seem complicated, but understanding it is crucial to ensuring a more secure economic future. Many people rely solely on state pension plans for their retirement, but is this enough? Additionally, investing in the stock market might seem risky for small investors, but with the right knowledge, it can be a powerful tool to grow your money. Below, we address these questions in simple terms.

Why You Should Invest in the Stock Market

1. Your Money Can Grow Faster

Keeping your money in a savings account has a downside: the interest it generates is often low and may not keep up with inflation (the increase in prices). This means your money loses value over time. On the other hand, investing in the stock market can offer much higher returns in the long term.

For example, stock markets have historically shown an average annual growth of 7-10%, far exceeding bank interest rates. While stock investments have ups and downs, the long-term outlook tends to be positive.

2. Financial Independence

Investing gives you control over your financial future. You don't have to depend solely on an employer, the government, or any other institution. Through investing, you can build a source of passive income that provides peace of mind.

Why Pension Plans Are Not Enough

1. Sustainability Issues

State pension systems face serious problems in many countries due to factors such as:

- Aging population: There are more retirees and fewer active workers to sustain the system.

- Inflation: Pension payments often lose purchasing power over time.

- Economic crises: Governments may face budget deficits, affecting pension funds.

This means relying solely on a state pension plan may not be sufficient to ensure a comfortable retirement.

Source: @BrianFeroldi (X), https://brianferoldi.kit.com/99

2. Depending Exclusively on the State Is Risky

Imagine depending entirely on something that might not be enough or could even disappear. Diversifying your income sources through investing is a smart way to protect yourself.

The Main Fears of Small Investors

Investing can be intimidating, especially if you're not familiar with financial markets. Here are the most common fears and how to address them:

1. “I’ll lose all my money”

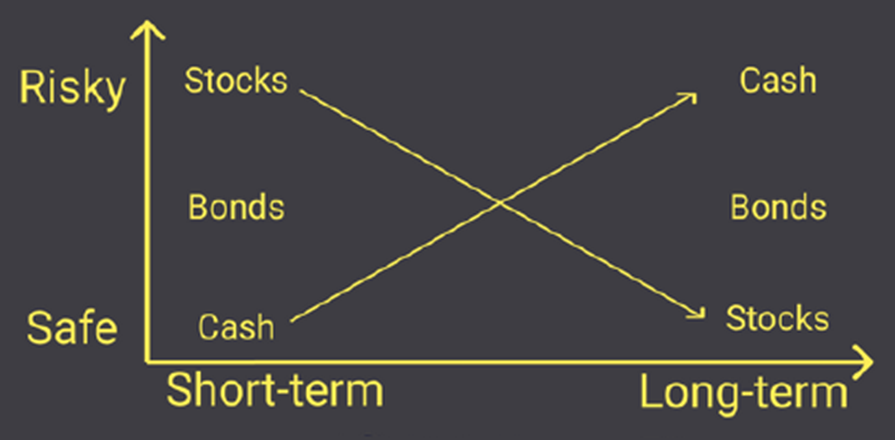

It’s natural to fear losses, but here’s the key: diversify your investments. Don’t put all your money into a single stock or sector. Also, remember that stock markets fluctuate; short-term losses are normal, but the goal is long-term growth.

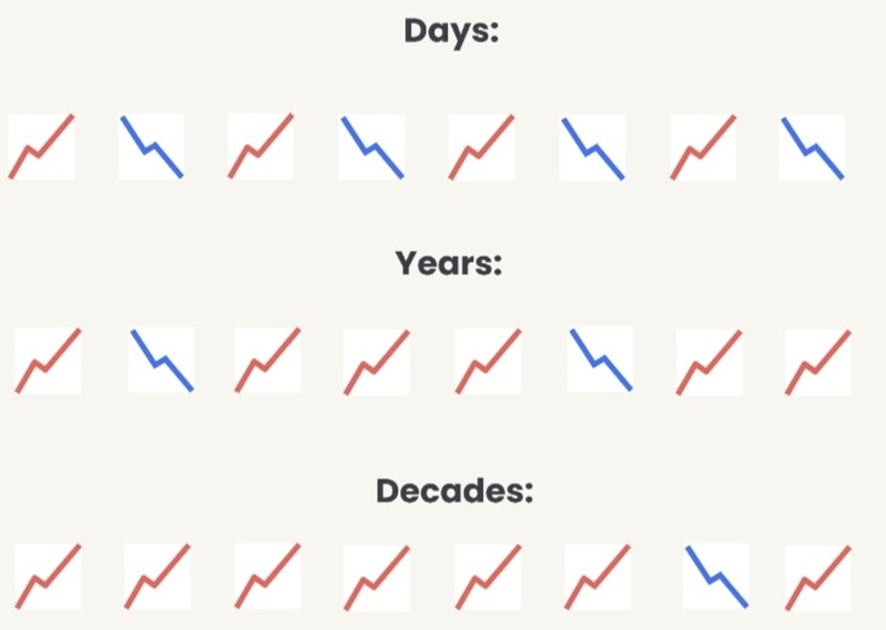

In this image we can see that there is always a reason to sell (fear) and that most of them are not even appreciated in the graph, the market falls are usually abrupt and short, and what can fall -40/-50%, yes it seems a lot, but years later are +300/+500%, then it was a lot or not? When more time on the stock exchange more may be those rises of 100% and no, that is not why it is a bubble, are companies increasingly earning more and more, and more and more money.

In this image, we can observe how the duration of market downturns is relatively short in most cases, and when there have been major downturns or much longer durations—around 30% of the cases—the market has recovered, offering higher returns. This is impossible to predict, at least for 99% of investors, and the other 1% gets it right occasionally. Therefore, in the face of a market downturn, there are only two options:

- HOLD ON

- DCA (strategy: Dollar Cost Average). That is, allocate a small portion of your savings to buying a little every month during these bearish market periods. You won’t hit the bottom price on all trades, but at least on some, you will.

2. “I don’t know anything about the stock market”

Many people don’t invest because they feel they lack the necessary knowledge. The solution is to learn the basics. Today, there are countless free resources, from online videos to beginner-friendly courses.

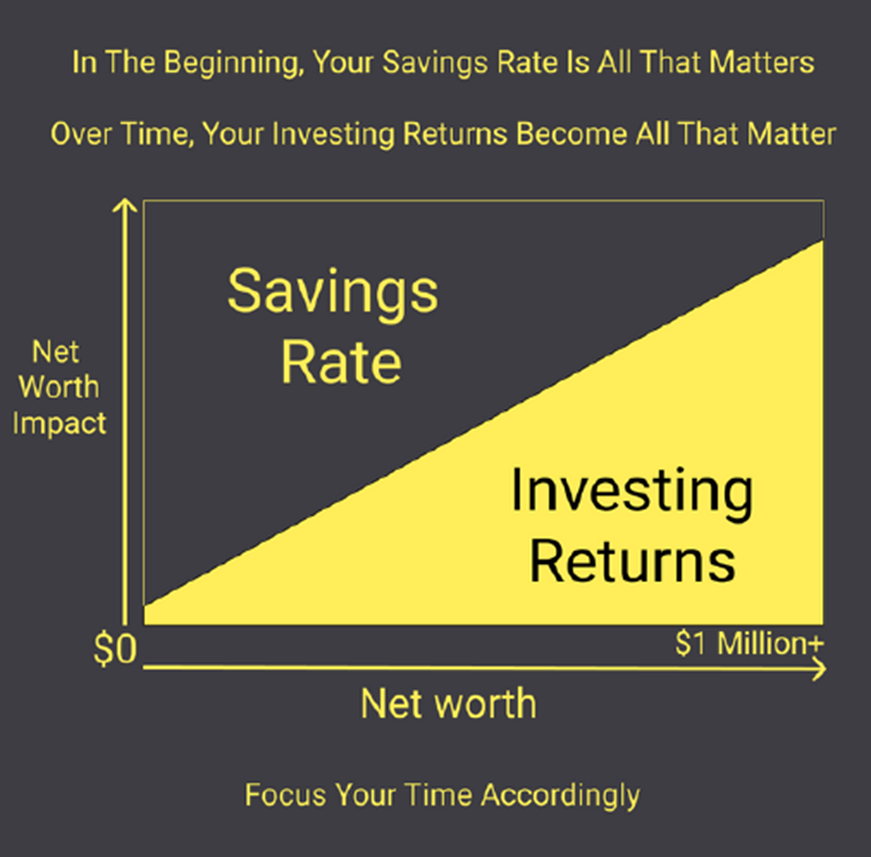

3. “I don’t have enough money to invest”

False! Nowadays, many platforms allow you to start with very small amounts. Additionally, by investing regularly, even small sums can grow significantly over time thanks to compound interest (interest earned on previously earned interest).

Source: @BrianFeroldi (X), https://brianferoldi.kit.com/99

How to Overcome These Fears

1. Basic Financial Education

Learning the basics of investing is the first step to feeling more confident. Dedicate a little time each week to reading or watching content about personal finance.

2. Start Small

You don’t need to start by investing large amounts. Begin with an amount you’re comfortable risking and gradually increase it as you feel more confident.

3. Invest for the Long Term

Avoid the temptation of “getting rich quickly.” The best strategies focus on holding investments for several years, allowing them to grow over time.

La Inflación "el impuesto a los pobres” (el principal motivo para invertir)

1. Impacto desproporcionado sobre ingresos bajos:

- Los hogares con ingresos bajos gastan una mayor proporción de su dinero en bienes básicos como alimentos, transporte y vivienda, cuyos precios suelen aumentar más rápidamente durante períodos de inflación.

- Los ricos, en cambio, suelen tener activos que pueden ajustarse o beneficiarse con la inflación, como bienes raíces, acciones o inversiones que preservan su valor.

2. Erosión del poder adquisitivo:

- La inflación reduce el valor real del dinero, afectando especialmente a quienes tienen ingresos fijos, como trabajadores asalariados o jubilados.

- Mientras los precios suben, los ingresos de estos grupos no siempre aumentan al mismo ritmo, deteriorando su calidad de vida.

3. Mayor dificultad para ahorrar:

- Para los pobres, que suelen tener acceso limitado a instrumentos de inversión, mantener ahorros en efectivo significa que su valor disminuye con la inflación.

- Los grupos más adinerados pueden proteger sus ahorros mediante inversiones que generan rendimientos reales positivos.

Beneficios para los Estados:

1. Reducción del valor real de la deuda pública:

- La inflación reduce el valor real de las deudas, incluyendo la deuda pública. Si los gobiernos tienen deudas significativas, pueden devolverlas con "dinero más barato" en términos reales, disminuyendo la carga relativa.

2. Incremento en la recaudación fiscal:

- Aunque los salarios y precios suben con la inflación, esto puede empujar a las personas a escalas más altas de impuestos sobre la renta en sistemas fiscales progresivos, aumentando la recaudación sin necesidad de cambios explícitos en las tasas impositivas.

- Lo mismo ocurre con impuestos indirectos como el IVA, que aumentan en términos absolutos al incrementarse los precios de los bienes.

3. Monetización del déficit:

- En algunos casos, los gobiernos pueden financiar déficits presupuestarios imprimiendo dinero, lo cual provoca inflación. Aunque esta práctica puede ser dañina a largo plazo, permite a los gobiernos solventar necesidades inmediatas.

4. Estímulo al consumo:

- La inflación moderada puede incentivar a los consumidores a gastar más rápidamente, temiendo que los precios sigan subiendo. Esto puede reactivar la economía y aumentar los ingresos fiscales indirectos.

Dilema ético y económico:

Aunque los Estados pueden beneficiarse de la inflación en ciertas circunstancias, esta genera una redistribución regresiva de la riqueza que afecta más a los sectores vulnerables. Por ello, una inflación alta y descontrolada suele ser vista como un fenómeno perjudicial que necesita regulación mediante políticas monetarias y fiscales.

La inflación actúa como un "impuesto" oculto que afecta más a los pobres debido a su incapacidad para protegerse de la erosión del poder adquisitivo. Por otro lado, los Estados pueden aprovechar ciertos efectos de la inflación para reducir sus cargas financieras y aumentar ingresos fiscales. Sin embargo, estos beneficios no justifican las consecuencias sociales negativas asociadas con una inflación elevada.

Conclusion

Investing in the stock market isn’t as complicated or risky as many think. It’s a tool that, when used wisely, can help you achieve greater financial stability and reduce your dependence on state pension systems that may not be sustainable. The key is to educate yourself, start small, and always think long-term.

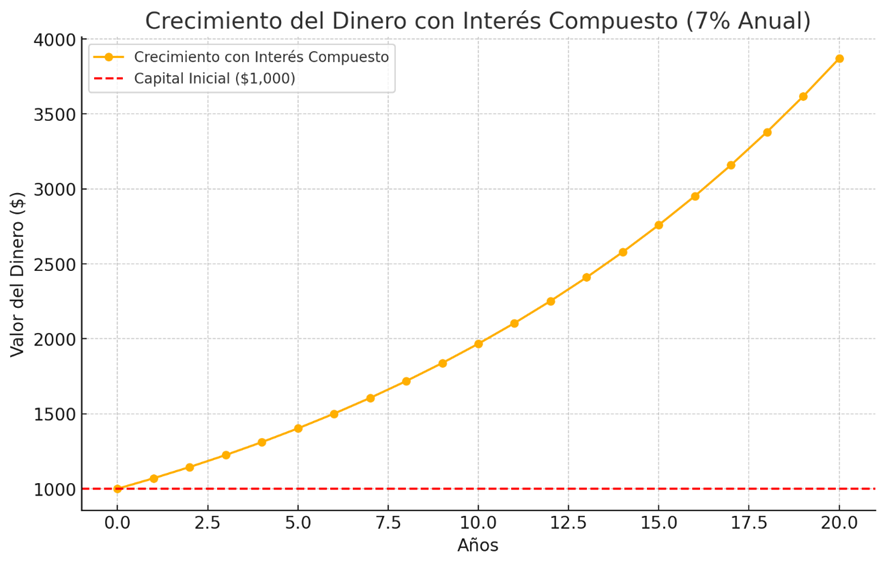

The graph illustrates the growth of money with compound interest at a 7% annual rate over 20 years. Starting with an initial capital of $1,000, the value increases significantly over time. This highlights the power of long-term investing.

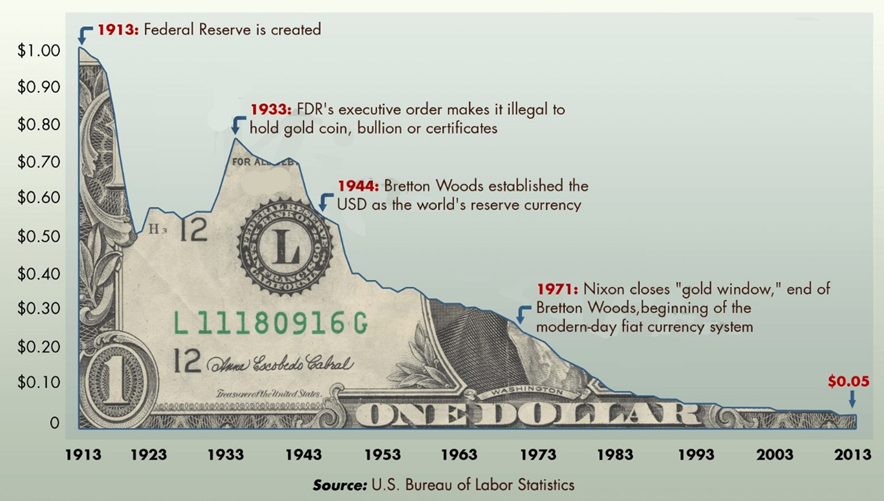

Devaluation of 1$ over the course of history.

Don't let this happen to your savings.

Glossary

- Inflation: The general increase in the prices of goods and services in an economy.

- Compound interest: Interest earned on both the initial principal and previously earned interest.

- Diversify: To invest in different assets to reduce risk.