Introduction to investment

Why Should Average People Invest in the Stock Market Instead of Relying on State Pension Plans?

The financial world may seem complicated, but understanding it is crucial to ensuring a more secure economic future. Many people rely solely on state pension plans for their retirement, but is this enough? Additionally, investing in the stock market might seem risky for small investors, but with the right knowledge, it can be a powerful tool to grow your money. Below, we address these questions in simple terms.

Why You Should Invest in the Stock Market

1. Your Money Can Grow Faster

Keeping your money in a savings account has a downside: the interest it generates is often low and may not keep up with inflation (the increase in prices). This means your money loses value over time. On the other hand, investing in the stock market can offer much higher returns in the long term.

For example, stock markets have historically shown an average annual growth of 7-10%, far exceeding bank interest rates. While stock investments have ups and downs, the long-term outlook tends to be positive.

2. Financial Independence

Investing gives you control over your financial future. You don't have to depend solely on an employer, the government, or any other institution. Through investing, you can build a source of passive income that provides peace of mind.

Why Pension Plans Are Not Enough

1. Sustainability Issues

State pension systems face serious problems in many countries due to factors such as:

- Aging population: There are more retirees and fewer active workers to sustain the system.

- Inflation: Pension payments often lose purchasing power over time.

- Economic crises: Governments may face budget deficits, affecting pension funds.

This means relying solely on a state pension plan may not be sufficient to ensure a comfortable retirement.

Source: @BrianFeroldi (X), https://brianferoldi.kit.com/99

2. Depending Exclusively on the State Is Risky

Imagine depending entirely on something that might not be enough or could even disappear. Diversifying your income sources through investing is a smart way to protect yourself.

The Main Fears of Small Investors

Investing can be intimidating, especially if you're not familiar with financial markets. Here are the most common fears and how to address them:

1. “I’ll lose all my money”

It’s natural to fear losses, but here’s the key: diversify your investments. Don’t put all your money into a single stock or sector. Also, remember that stock markets fluctuate; short-term losses are normal, but the goal is long-term growth.

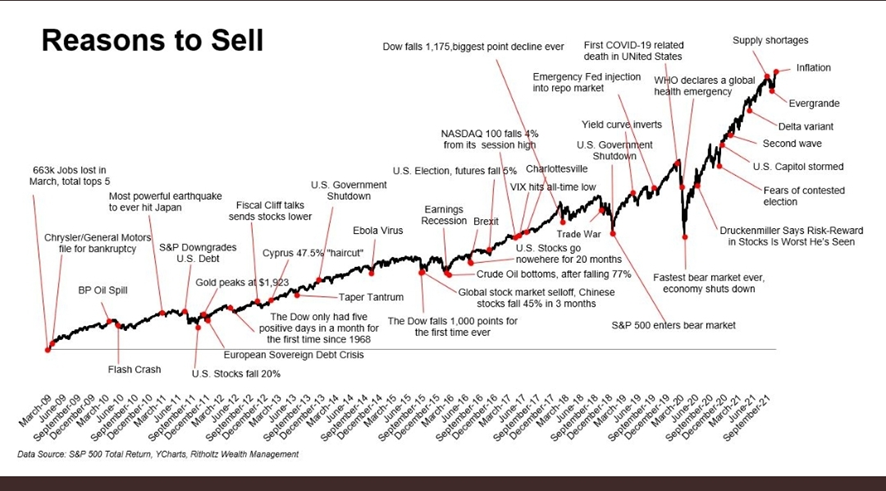

In this image we can see that there is always a reason to sell (fear) and that most of them are not even appreciated in the graph, the market falls are usually abrupt and short, and what can fall -40/-50%, yes it seems a lot, but years later are +300/+500%, then it was a lot or not? When more time on the stock exchange more may be those rises of 100% and no, that is not why it is a bubble, are companies increasingly earning more and more, and more and more money.

In this image, we can observe how the duration of market downturns is relatively short in most cases, and when there have been major downturns or much longer durations—around 30% of the cases—the market has recovered, offering higher returns. This is impossible to predict, at least for 99% of investors, and the other 1% gets it right occasionally. Therefore, in the face of a market downturn, there are only two options:

- HOLD ON

- DCA (strategy: Dollar Cost Average). That is, allocate a small portion of your savings to buying a little every month during these bearish market periods. You won’t hit the bottom price on all trades, but at least on some, you will.

2. “I don’t know anything about the stock market”

Many people don’t invest because they feel they lack the necessary knowledge. The solution is to learn the basics. Today, there are countless free resources, from online videos to beginner-friendly courses.

3. “I don’t have enough money to invest”

False! Nowadays, many platforms allow you to start with very small amounts. Additionally, by investing regularly, even small sums can grow significantly over time thanks to compound interest (interest earned on previously earned interest).

Source: @BrianFeroldi (X), https://brianferoldi.kit.com/99

4. How to Overcome These Fears

4.1 Basic Financial Education

Learning the basics of investing is the first step to feeling more confident. Dedicate a little time each week to reading or watching content about personal finance.

4.2 Start Small

You don’t need to start by investing large amounts. Begin with an amount you’re comfortable risking and gradually increase it as you feel more confident.

4.3 Invest for the Long Term

Avoid the temptation of “getting rich quickly.” The best strategies focus on holding investments for several years, allowing them to grow over time.

Inflation: "The Tax on the Poor" (The Main Reason to Invest)

1. Disproportionate Impact on Low Incomes:

- Low-income households spend a larger proportion of their money on basic necessities such as food, transportation, and housing, whose prices tend to rise more rapidly during inflationary periods.

- The wealthy, on the other hand, often hold assets that can adjust to or benefit from inflation, such as real estate, stocks, or investments that preserve their value.

2. Erosion of Purchasing Power:

- Inflation reduces the real value of money, especially affecting those with fixed incomes, such as salaried workers or retirees.

- As prices rise, the incomes of these groups do not always increase at the same pace, deteriorating their quality of life.

3. Greater Difficulty in Saving:

- For the poor, who often have limited access to investment instruments, keeping savings in cash means their value declines with inflation.

- Wealthier groups can protect their savings through investments that generate positive real returns.

Benefits for Governments:

1. Reduction in the Real Value of Public Debt:

- Inflation decreases the real value of debts, including public debt. If governments have significant debt, they can repay it with "cheaper money" in real terms, reducing the relative burden

2. Increase in Tax Revenue:

- As wages and prices rise with inflation, people may be pushed into higher income tax brackets in progressive tax systems, increasing government revenue without explicit tax rate changes.

- The same applies to indirect taxes like VAT, which increase in absolute terms as the prices of goods rise.

3. Deficit Monetization:

- In some cases, governments can finance budget deficits by printing money, which causes inflation. While this practice can be harmful in the long run, it allows governments to cover immediate financial needs.

4. Stimulus to Consumption:

- Moderate inflation can encourage consumers to spend more quickly, fearing that prices will continue to rise. This can boost economic activity and increase indirect tax revenues.

Ethical and Economic Dilemma:

Although governments can benefit from inflation under certain circumstances, it generates a regressive redistribution of wealth that disproportionately affects vulnerable sectors. Therefore, high and uncontrolled inflation is generally seen as a harmful phenomenon that requires regulation through monetary and fiscal policies.

Inflation acts as a hidden "tax" that primarily affects the poor due to their inability to protect themselves from the erosion of purchasing power. On the other hand, governments can take advantage of some inflationary effects to reduce their financial burdens and increase tax revenues. However, these benefits do not justify the negative social consequences associated with high inflation.

5. Conclusion:

Investing in the stock market isn’t as complicated or risky as many think. It’s a tool that, when used wisely, can help you achieve greater financial stability and reduce your dependence on state pension systems that may not be sustainable. The key is to educate yourself, start small, and always think long-term.

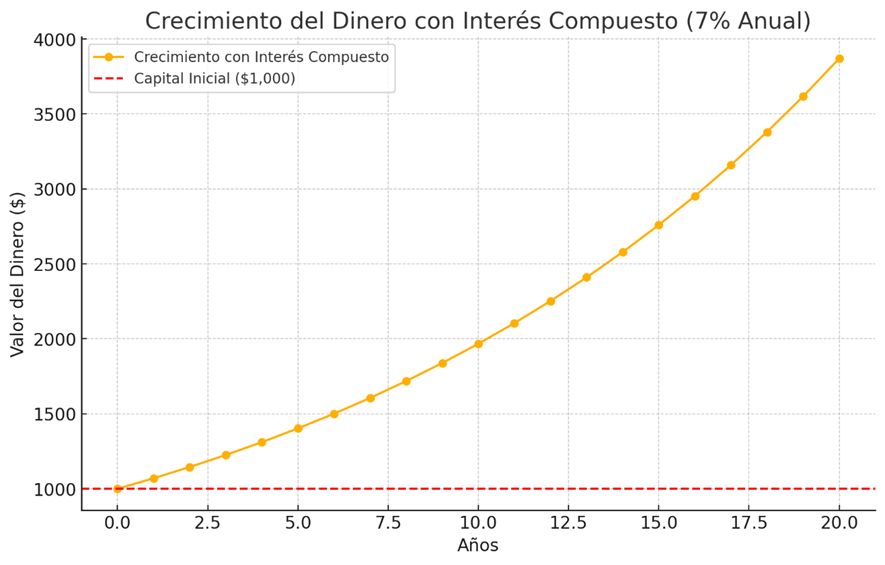

The graph illustrates the growth of money with compound interest at a 7% annual rate over 20 years. Starting with an initial capital of $1,000, the value increases significantly over time. This highlights the power of long-term investing.

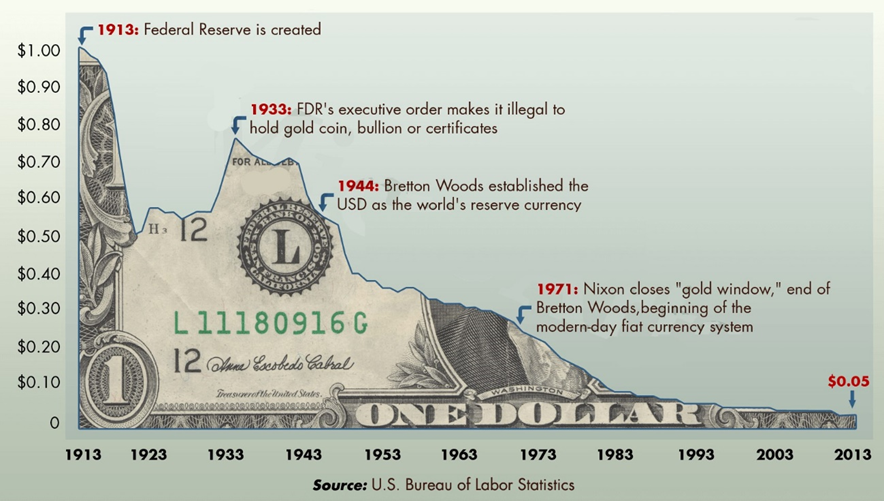

6. Devaluation of 1$ over the course of history.

Don't let this happen to your savings.

7. Glossary

- Inflation: The general increase in the prices of goods and services in an economy.

- Compound interest: Interest earned on both the initial principal and previously earned interest.

- Diversify: To invest in different assets to reduce risk.